Looking For More Great Content?

Get even more informative Toronto real estate news sent directly to your inbox by signing up for my newsletter here. All it takes is a few easy clicks.

Avoiding Capital Gains Tax on Property Sale in Canada: A 2026 Strategic Guide

03/13/26 Uncategorized

What if the recent shift to a 66.67% inclusion rate on gains over C$250,000 didn’t have to erode your hard-earned equity? Since the federal government updated these tax thresholds on June 25, 2024, many homeowners feel a growing sense of anxiety about protecting their financial legacy. You’ve likely spent years maintaining your property and watching the market grow; seeing a large portion of that effort diverted to the CRA can feel like a major setback to your retirement or your next purchase. At Noble Real Estate, we believe that avoiding capital gains tax on property sale canada should be a straightforward process built on analytical rigour and professional guidance.

This approach of integrating expert financial and real estate advice is crucial for homeowners across Canada. In British Columbia, for example, many sellers seek out the expertise of a professional like Alex Mazhari PREC to ensure their transactions are structured in the most tax-efficient way.

We’re here to ensure you feel knowledgeable and supported as you prepare for your next move. In this 2026 strategic guide, you’ll discover the legal exemptions and actionable steps available to minimize or eliminate your tax burden. We’ll explore the Principal Residence Exemption in detail, provide a checklist for increasing your Adjusted Cost Base through documented capital improvements, and outline a clear roadmap for a successful sale. By applying “The Noble Approach,” you can transform a complex tax situation into a manageable part of your overall financial strategy.

Key Takeaways

- Discover how to fully utilize the Principal Residence Exemption and the “plus one” rule to protect your home’s equity from taxation.

- Navigate the 2026 tax changes by understanding how the C$250,000 annual threshold impacts your strategy for avoiding capital gains tax on property sale canada.

- Master the art of strategic designation between primary and secondary properties to minimize the tax burden on your cherished family cottage.

- Explore sophisticated methods like the Capital Gain Reserve and loss offsetting to spread your tax liabilities over multiple years and retain more of your investment.

- Experience “The Noble Approach,” where CPA-led financial insights are integrated into your home valuation to ensure a stress-free and fiscally optimized sale.

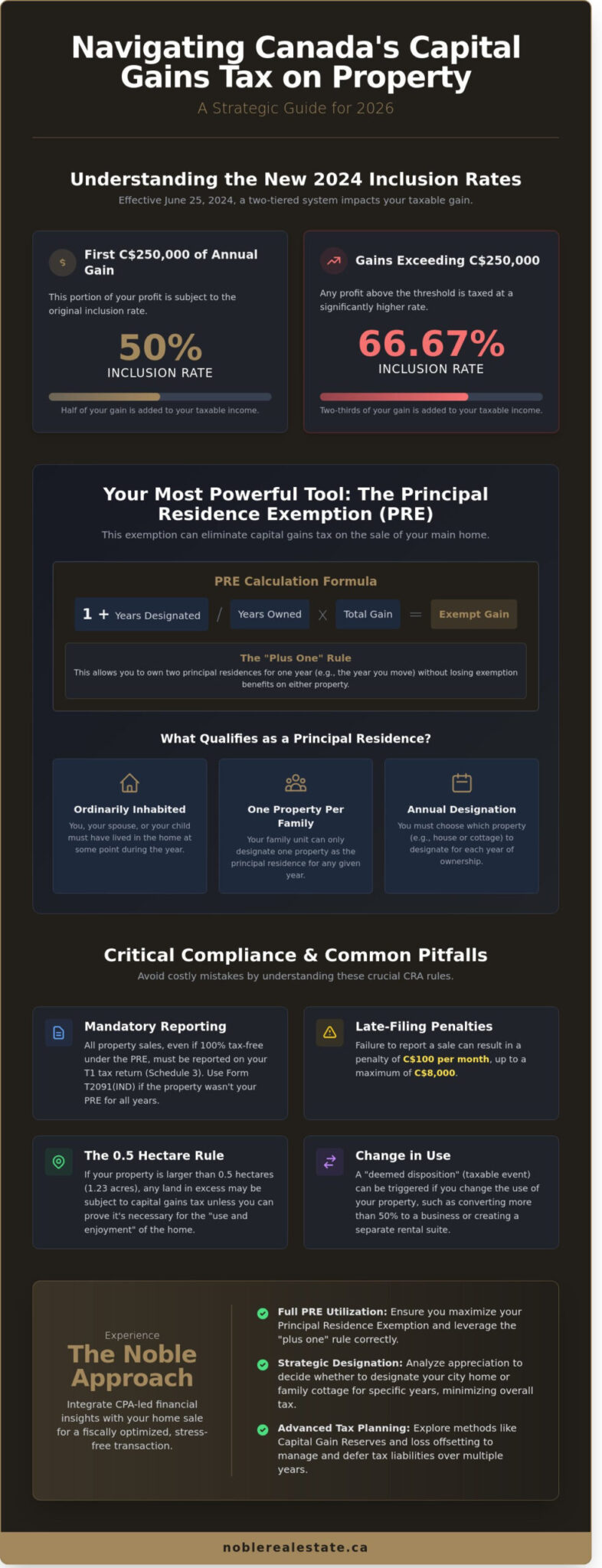

The Principal Residence Exemption: Your Most Powerful Tax Tool

Selling your home represents a major financial milestone. It’s often your largest asset, and protecting the equity you’ve built is a top priority. The Noble Approach focuses on ensuring you keep as much of that profit as possible through analytical rigor and a deep understanding of tax regulations. For most homeowners, the Principal Residence Exemption (PRE) is the primary vehicle for avoiding capital gains tax on property sale canada. This rule allows you to eliminate tax liability on the gain realized from the sale of your home, provided it meets specific criteria set by the Canada Revenue Agency (CRA).

The CRA uses a specific formula to calculate this exemption, which includes a “plus one” rule. The formula is (1 + Number of years designated) divided by (Number of years owned) multiplied by the total gain. That “plus one” is a generous provision. It ensures that if you buy a new home and sell your old one in the same calendar year, you don’t lose a year of eligibility on either property. It’s a small detail that provides a significant buffer for families in transition.

Since October 3, 2016, the CRA requires every homeowner to report the sale of a principal residence on their income tax return. Even if your sale is 100% tax-free, silence is no longer an option. Understanding the broader context of Capital Gains Taxation in Canada helps clarify why these reporting rules exist. They’re designed to prevent system abuse and ensure only legitimate residences receive the tax-free status.

What Qualifies as a Principal Residence in Canada?

To qualify, you, your spouse, or your child must have “ordinarily inhabited” the home at some point during the calendar year. Your family unit, which includes your spouse and children under 18, can only designate one property as a principal residence for any given year. This rule applies to seasonal properties too. If you own a cottage in the Uxbridge area and a house in the city, you must choose which one to designate for each year of ownership. If the cottage appreciated more in value, designating it for certain years might be the smarter financial move.

Reporting the Sale: Form T2091(IND)

You must complete Schedule 3 of your T1 Income Tax and Benefit Return to report the sale. If the property wasn’t your principal residence for every year you owned it, you’ll also need Form T2091(IND). This is the technical side of avoiding capital gains tax on property sale canada correctly. Missing this filing is costly. The CRA can levy a late-filing penalty of C$100 for each month the form is late, reaching a maximum of C$8,000. If you forgot to report a past sale, you can request an amendment under the Voluntary Disclosures Program, though the penalty may still apply.

Watch out for common pitfalls like the 0.5-hectare rule. If your property exceeds 1.23 acres, the CRA may tax the portion of the land not required for the “use and enjoyment” of the home. Using more than 50% of your home for business or making structural changes to create a rental suite can also trigger a partial change in use. These scenarios can create a surprise tax bill if you aren’t prepared. My goal is to make these complex processes feel straightforward, ensuring your transition is as successful and stress-free as possible.

Understanding the 2026 Capital Gains Inclusion Rates

The Canadian tax landscape shifted significantly on June 25, 2024, creating a two-tiered system that directly impacts your 2026 real estate strategy. For individuals, the first C$250,000 of capital gains realized in a calendar year continues to be taxed at a 50% inclusion rate. However, any profit exceeding that C$250,000 threshold is now subject to a higher inclusion rate of 66.67%. This change makes the timing of your sale a primary factor in avoiding capital gains tax on property sale canada by staying within the lower inclusion bracket whenever possible.

2026 is a critical year for many property owners because it marks the second full year under these intensified rules. If you’re planning to liquidate a high-value investment or a secondary cottage, the difference between a single sale and a staggered disposition could represent a 16.67% difference in taxable income. This isn’t just a minor adjustment; it’s a structural change that requires a seasoned, financially savvy approach to protect your home equity.

Calculating Your Taxable Capital Gain

Determining your tax liability starts with a clear formula: your Proceeds of Disposition (the sale price minus commissions and legal fees) minus your Adjusted Cost Base (ACB). The inclusion rate is the portion of the profit that is added to your taxable income. For example, if an Uxbridge seller realizes a C$500,000 gain on a secondary property, the calculation is no longer a simple flat rate. The first C$250,000 results in C$125,000 of taxable income, while the next C$250,000 results in roughly C$166,675 of taxable income. You can significantly reduce these figures if the property qualifies for the principal residence exemption, which remains the most effective tool for tax elimination in the Canadian market.

Individual vs. Corporate Ownership

The 2026 rules are particularly stringent for properties held within a corporation. Unlike individual owners, corporations do not benefit from the C$250,000 threshold at the 50% rate. Every dollar of capital gain realized by a corporation or a holding company is taxed at the 66.67% inclusion rate from the very first cent. This makes investment properties held in a “Holdco” more expensive to sell than those held personally.

- Holdco Impact: A C$300,000 gain in a corporation results in C$200,010 of taxable income, whereas an individual would only face C$158,342 for the same gain.

- Strategic Timing: If you own multiple units, consider selling them in different tax years to maximize the annual C$250,000 limit for personal holdings.

- Portfolio Review: 2026 is an ideal time to assess whether your corporate-held assets should be restructured before further appreciation occurs.

Managing high-value sales requires more than just a “For Sale” sign; it demands an analytical understanding of how these thresholds interact with your total annual income. Using the Noble Approach, we look at your entire financial picture to ensure your real estate goals align with your tax obligations. If you’re curious about how your specific property fits into the current market, you can get in touch for a comprehensive evaluation. Staying informed and proactive is the only way to ensure your transition remains stress-free and financially sound.

Minimizing Tax on Secondary Properties and Cottages

One of the most effective strategies involves the “plus one” rule for principal residence designations. You can choose which property to designate as your principal residence for specific years of ownership. If your cottage has appreciated by C$30,000 per year while your city home has only grown by C$15,000 per year, it’s often smarter to designate the cottage for those years. This requires a careful analysis of the total capital gain over the entire holding period to ensure you’re protecting the largest pool of equity. My background as a CPA allows me to help clients run these exact numbers to find the most tax-efficient path.

If you’ve lived in a home and later decided to rent it out, you’ve triggered a “change in use.” The CRA views this as a deemed disposition, meaning they treat it as if you sold the property at its current fair market value. You might face a tax bill even if no actual sale occurred. However, you can often file a subsection 45(2) election. This special tax filing allows you to maintain the property as your principal residence for up to four additional years while it’s a rental, provided you don’t designate another home during that time. This is a common scenario for Durham Region homeowners moving from a starter townhome into a larger detached property while keeping the first as an investment.

Maximizing Your Adjusted Cost Base (ACB)

Your Adjusted Cost Base is the total amount you’ve invested in the property. A higher ACB means a smaller taxable gain. You should review the Canada Revenue Agency (CRA) definitions for capital gains to see which costs are eligible. Keep every receipt for major projects like a C$20,000 roof replacement, a C$50,000 kitchen remodel, or the installation of a C$15,000 HVAC system. Don’t forget that selling costs also reduce your gain. This includes real estate commissions, which can be 5% of the sale price, and legal fees that typically range from C$1,500 to C$2,500.

Partial Exemptions for Multi-Use Properties

Properties in Uxbridge often sit on large parcels of land, which brings the 1/2 hectare rule into play. The CRA generally only exempts the portion of your land that is “necessary” for the use of the home, typically capped at 1.24 acres. If you’re selling a 10-acre hobby farm for development, the gain on the house and the first 1.24 acres might be tax-free, but the remaining 8.76 acres will likely be subject to tax. Similar rules apply if you run a business or a rental suite out of your home. If you’ve claimed capital cost allowance (depreciation) on a home office, you may lose the ability to claim the principal residence exemption on that specific portion of the property.

Strategic Timing and Loss Offsetting Strategies

Timing a sale isn’t just about watching the Uxbridge market trends; it’s about managing the CRA calendar. When you sell an investment property, the resulting tax bill can be a heavy burden if managed poorly. By utilizing specific provisions within the Income Tax Act, you can soften the blow and keep more of your hard-earned equity. Strategic planning is a core part of avoiding capital gains tax on property sale canada, especially for high-value transactions that exceed the new thresholds set in 2024.

The 5-Year Capital Gain Reserve

If you don’t require the entire sale amount upfront, a Vendor-Take-Back (VTB) mortgage allows you to defer your tax liability. Under Section 40(1) of the Income Tax Act, you can claim a capital gain reserve if a portion of the sale price is payable after the end of the year. You’re required to report a minimum of 20% of the gain each year, which effectively spreads the tax over a five-year period. This strategy is highly effective for Uxbridge sellers moving large rural properties or commercial lots where buyers might need creative financing. It prevents you from being pushed into the highest tax bracket by distributing the income over several years instead of one massive spike in a single filing period.

Tax-Loss Harvesting for Real Estate Sellers

Your real estate investments should work in tandem with your broader financial portfolio. If you anticipate a large gain from a property sale, look for underperforming assets in your brokerage accounts. Selling stocks or mutual funds that have dropped in value creates a capital loss that can offset your real estate gains. Since the Canadian government increased the capital gain inclusion rate to 66.67% for gains exceeding C$250,000 for individuals on June 25, 2024, this tactic has become essential. You can also carry capital losses back three years to recover taxes paid previously or carry them forward indefinitely to use against future sales. Aligning these moves requires a sharp eye for detail. As a CPA, Colin Noble integrates this financial rigour into every transaction, ensuring your portfolio remains balanced.

- Avoid Multi-Asset Sales: Selling two investment properties in the same tax year can be a costly mistake. It often triggers the 66.67% inclusion rate on the portion above C$250,000. Spacing these sales across December and January can save you thousands in tax.

- Charitable Donations: Donating publicly traded shares or ecologically sensitive land to a registered charity results in a 0% capital gains inclusion rate. This is a sophisticated way to give back while protecting your wealth.

- Strategic Offsetting: Ensure your losses are realized in the same calendar year as your gain to maximize the immediate impact on your tax return.

Managing these moving parts requires more than just a standard real estate agent. It requires an analytical mindset that treats your property as the significant financial asset it is. We help you look at the big picture to ensure your transition is both profitable and protected from unnecessary tax erosion. To see how we can optimize your upcoming sale with professional precision, explore The Noble Approach for a comprehensive, finance-first perspective.

The Noble Approach: Professional Guidance for Your Sale

Selling a property involves more than just a “For Sale” sign and a few open houses. It requires a deep dive into your financial portfolio to ensure the equity you have built over years remains in your pocket. When you work with a real estate team led by a Chartered Professional Accountant (CPA), you gain a level of analytical rigour that standard services simply cannot provide. We call this the Noble Advantage. It means we don’t just guess at your potential profit; we calculate your actual net-in-pocket figure by accounting for commissions, legal fees, and potential tax liabilities from the very first meeting.

This financial lens is vital for anyone focused on avoiding capital gains tax on property sale canada. Most agents focus solely on the top-line sale price. Our approach prioritizes your bottom-line result. By integrating tax planning into the initial home valuation, we help you understand the true financial impact of a sale before you ever sign a listing agreement. This foresight allows for better decision-making regarding timing, capital improvements, and reinvestment strategies.

Financial Rigour Meets Real Estate Excellence

Precise numbers matter more than ever in the current regulatory environment. Since June 25, 2024, the inclusion rate for capital gains over C$250,000 has increased to 66.7 percent for individuals. This change makes avoiding capital gains tax on property sale canada a primary concern for many investors and second-home owners. Colin Noble’s background as a CPA/CA changes the conversation from “what can we sell for” to “how much will you keep.” We help you identify eligible expenses that can be added to your adjusted cost base (ACB), such as major renovations or legal costs, which directly reduces the taxable portion of your gain.

Our local expertise in Uxbridge and the surrounding Durham Region is another pillar of this financial rigour. Accurate property valuations are not just about finding a buyer; they are about establishing a defensible fair market value for the CRA if you are changing the use of a property from a primary residence to a rental. Understanding the specific market trends in our community allows us to position your home effectively while planning for the tax implications of the final sale price. You can start this process today by discovering What’s My Uxbridge Home Really Worth? through our detailed assessment tool.

Preparing for a Stress-Free Closing

A successful sale doesn’t end when the keys change hands. Our end-to-end approach ensures you are prepared for the following tax season long before the deadline approaches. We emphasize collaboration with your existing circle of professionals, including your personal accountant and lawyer, before the deal becomes firm. This proactive communication ensures that all parties are aligned on the structure of the sale and that no detail is overlooked during the closing process.

We help you organize the necessary documentation for your 2026 tax return if you are selling in 2025. This includes maintaining records of the Principal Residence Exemption (PRE) forms and tracking all selling costs that can be deducted. Our goal is to make the transition as straightforward as possible by providing:

- Detailed breakdowns of net proceeds after all C$ costs.

- Strategic advice on the timing of the sale to optimize tax brackets.

- Comprehensive support in gathering records for your adjusted cost base.

- Expert guidance on CRA reporting requirements for real estate transactions.

Take the first step toward a successful transaction by choosing a team that understands the numbers as well as the neighbourhood. Book a Strategic Consultation to ensure your next move is your smartest financial move yet.

Maximize Your Home Equity in 2026 and Beyond

Navigating the shifting tax landscape requires more than just basic knowledge; it demands a proactive strategy. By maximizing your Principal Residence Exemption and understanding how the 2026 inclusion rates affect your bottom line, you can protect your hard-earned equity. Strategic timing and loss offsetting aren’t just suggestions. They’re essential components of avoiding capital gains tax on property sale canada when dealing with secondary residences or investment properties. Your equity matters.

Success in the Durham Region market shouldn’t feel like a gamble. Led by Colin Noble, a CPA and CA with extensive financial experience, our team brings analytical rigour to every transaction in Uxbridge and the surrounding areas. We replace uncertainty with the Noble Approach, a personalized method designed to make your transition stress-free. You don’t have to navigate these complex 2026 regulations alone. Expert guidance ensures you keep more of your investment where it belongs.

Redefine your expectations-start your strategic home sale with Noble Real Estate today

Your financial goals are within reach when you have a seasoned expert leading the way.

Frequently Asked Questions

Can I avoid capital gains tax if I sell my cottage in Ontario?

You can eliminate capital gains tax on your cottage sale by designating it as your principal residence for the years you owned it. Under Canadian tax law, a family unit can only designate one property per year as their primary home. If you choose the cottage, you’ll save on that sale but will eventually owe tax on your other home for those same years. The Noble Approach involves calculating which property has the higher accrued value to ensure you apply the exemption where it saves you the most money.

What is the capital gains inclusion rate in Canada for 2026?

The capital gains inclusion rate for 2026 follows the rules established on June 25, 2024. For individuals, the first C$250,000 of capital gains in a year are taxed at a 50% inclusion rate. Any gains exceeding that C$250,000 threshold are taxed at a 66.7% inclusion rate. Corporations and most trusts face a flat 66.7% inclusion rate on all capital gains. These figures represent the portion of the profit added to your taxable income for the year.

How does the CRA define a “principal residence”?

The CRA defines a principal residence as a housing unit that you, your spouse, or your child “ordinarily inhabit” during the calendar year. This definition includes detached houses, cottages, condominiums, and even houseboats. You must own the property alone or jointly with another person. It’s important to remember that since 1982, a family unit can designate only one property as a principal residence for any given year to qualify for the full tax exemption.

Do I have to pay tax if I sell my house and buy a cheaper one?

You don’t pay any tax on the profit from selling your primary home regardless of the price of your next property. The Principal Residence Exemption covers 100% of the gain on your main home, even if you’re downsizing from a C$1,500,000 house to a C$900,000 condo. Unlike some other countries, Canada doesn’t require you to “roll over” the profit into a new purchase to avoid taxation. This makes the transition to a smaller home in Uxbridge or the surrounding areas straightforward and financially predictable.

What expenses can I deduct from my capital gains on a property sale?

You can deduct outlays and expenses related to the sale, including real estate commissions which typically average 5%, legal fees, and advertising costs. A major part of avoiding capital gains tax on property sale canada is accurately calculating your Adjusted Cost Base (ACB). This includes the original purchase price plus capital improvements like a C$15,000 kitchen renovation or a C$5,000 furnace replacement. Keeping receipts for every upgrade since your purchase date is essential for reducing your taxable profit.

How does the “change in use” rule work for rental properties?

A “change in use” occurs when you convert your primary home into a rental or vice versa, which the CRA views as a “deemed disposition” at fair market value. This means you’re treated as if you sold the house and bought it back immediately at its current price. However, you can file a Section 45(2) election to defer this gain for up to 4 years. This election is a professional strategy that helps maintain the property’s status as a principal residence even while it generates rental income.

Is there a lifetime capital gains exemption for real estate?

No, the Lifetime Capital Gains Exemption (LCGE) doesn’t apply to residential or commercial real estate investments. The 2024 LCGE limit of C$1,250,000 is reserved specifically for qualified small business corporation shares and qualified farm or fishing properties. For real estate, your primary tools for tax reduction remain the Principal Residence Exemption and the strategic tracking of capital expenditures. Professional guidance ensures you don’t miss these specific opportunities to protect your equity.

What happens if I inherit a property and then sell it?

When you inherit a property, you’re considered to have acquired it at its fair market value on the date of the previous owner’s death. If the property was worth C$750,000 when you inherited it in 2023 and you sell it for C$790,000 in 2025, you only pay tax on the C$40,000 increase. If you move into the home and make it your primary residence immediately, you may qualify for the Principal Residence Exemption for the period you own it. This ensures the transfer of family wealth remains as stress-free as possible.