Looking For More Great Content?

Get even more informative Toronto real estate news sent directly to your inbox by signing up for my newsletter here. All it takes is a few easy clicks.

How to Prepare Financially to Buy a Home in Ontario: A 2026 Strategy Guide

05/12/26 Uncategorized

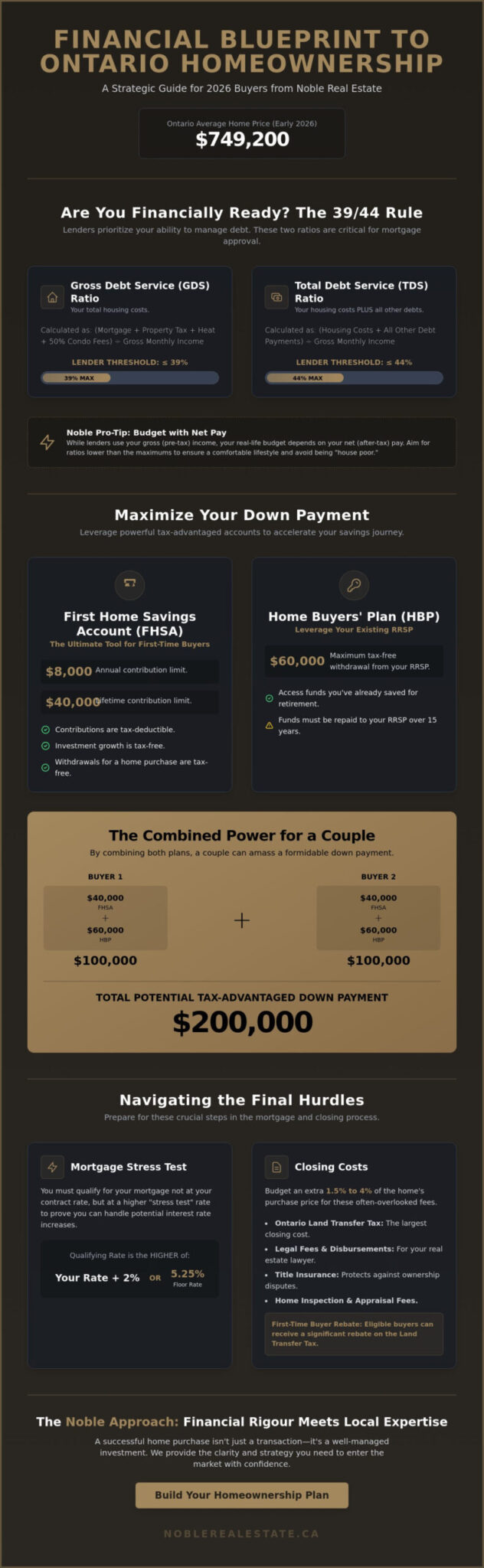

With Ontario’s average home price reaching $749,200 in early 2026, many aspiring buyers are discovering that a standard down payment is only one piece of a much larger puzzle. It’s no longer just about what you save, but how strategically you’ve structured your assets to meet modern lending requirements. Understanding exactly how to prepare financially to buy a home in Ontario is the difference between a rejected application and a successful closing in the Durham Region’s competitive market.

We know that the current financial landscape can feel overwhelming, especially with the 5.25% mortgage stress test floor and the complexity of various tax-advantaged accounts. You deserve a clear, analytical path that replaces uncertainty with a concrete plan of action. This guide shares the Noble Approach to homeownership, offering expert insights on maximizing your $60,000 RRSP Home Buyers’ Plan withdrawal and leveraging the $8,000 annual FHSA limit. We will break down the provincial land transfer tax tiers and hidden closing costs so you can step into your new home with absolute confidence and zero financial surprises.

Key Takeaways

- Understand the critical debt-to-income ratios lenders use and why the 39% housing cost rule is your most important benchmark for mortgage approval.

- Discover how to maximize the First Home Savings Account and the Home Buyers’ Plan to build a larger down payment using tax-free capital.

- Identify often overlooked closing costs, including Ontario’s provincial land transfer tax tiers and the specific rebates available to first-time buyers.

- Learn exactly how to prepare financially to buy a home in ontario by navigating the 2026 mortgage stress test and optimizing your credit profile.

- Apply a professional financial lens to your purchase, moving beyond a simple transaction to manage your home as a strategic real estate investment.

Determining Your Financial Readiness: The 39/44 Rule

Before you start browsing listings in Uxbridge or Pickering, you must understand the mathematical framework that dictates your buying power. Most buyers focus solely on their down payment, but lenders prioritize your ability to service debt over the long term. This is where the 39/44 rule becomes your most important roadmap. These numbers represent the maximum percentage of your income that can go toward debt, and staying within these limits is essential for a stress-free mortgage application. Understanding these benchmarks is a key part of navigating housing affordability in Canada, especially as lending criteria remain strict in 2026.

Learning how to prepare financially to buy a home in ontario starts with a rigorous audit of your current monthly obligations. Lenders use two specific ratios to decide if you’re a safe bet. The first is the Gross Debt Service (GDS) ratio, which covers your housing costs. The second is the Total Debt Service (TDS) ratio, which includes every other debt you carry. If these numbers are too high, even a large down payment might not save your application. You want to walk into a bank with the confidence that your numbers already align with their requirements.

Calculating Your GDS and TDS Ratios

Lenders calculate your GDS by adding up your monthly mortgage payments, property taxes, and heating costs. If you’re buying a condo, they also include 50% of the maintenance fees. You then divide this total by your gross monthly income. The magic number here is 39%. If your housing costs exceed 39% of what you earn before taxes, you’ll likely face a rejection or be asked for a significantly larger down payment.

The TDS ratio goes one step further by adding your other monthly debts to that housing total. This includes car loans, credit card minimums, and student debt. This total should not exceed 44% of your gross income. By performing this calculation yourself, you can see exactly where you stand. It’s often better to pay down a high-interest car loan before applying for a mortgage, as it directly improves your TDS and increases your total borrowing capacity.

The Reality of Gross Income vs. Net Take-Home Pay

One common pitfall for Ontario buyers is budgeting based on gross income rather than net take-home pay. While banks use your gross income for their formulas, you live on what’s left after taxes. In a high-tax province, this discrepancy is significant. With the 2026 interest rate environment still requiring a cautious approach, you don’t want to be “house poor” simply because you met the bank’s maximum threshold.

The Noble Approach emphasizes financial rigour, which means building a “buffer zone” into your personal budget. This extra space accounts for unexpected maintenance and the rising costs of utilities. A successful home purchase isn’t just about getting the keys; it’s about ensuring your lifestyle remains enjoyable after the move. Aiming for ratios slightly lower than the 39/44 maximum provides the flexibility you need to manage your home as a sound investment rather than a financial burden.

Strategic Saving: Maximizing Ontario and Federal Tax Incentives

Building your down payment in 2026 requires more than just discipline; it demands a tactical use of available tax shelters to accelerate your growth. When considering how to prepare financially to buy a home in ontario, the First Home Savings Account (FHSA) stands out as the premier tool for local buyers. With an annual contribution limit of $8,000 and a lifetime cap of $40,000, this account allows your money to grow entirely tax-free while providing a deduction on your income tax return. For a couple buying together, this represents a combined $80,000 in tax-advantaged capital, which is a significant portion of the down payment for the average $749,200 Ontario home.

The Home Buyers’ Plan (HBP) remains a vital secondary pillar, allowing you to withdraw up to $60,000 from your RRSP tax-free. Combined with the FHSA, a single buyer can access $100,000 plus any investment growth to fund their purchase. To reach these goals faster, many clients find success by automating their savings. Setting up a recurring transfer on payday ensures your home fund grows before you have the chance to spend those dollars elsewhere. If you’re looking for clarity on how these savings translate into real-world purchasing power, a professional home valuation of your current assets can provide a clear starting point.

The FHSA vs. RRSP HBP: Which Comes First?

Choosing where to put your first dollar depends on your timeline and tax bracket. The FHSA acts as a powerful hybrid of RRSP and TFSA benefits for 2026 buyers, offering tax-deductible contributions and tax-free withdrawals for your down payment. Unlike the HBP, you don’t have to pay back the funds you withdraw from an FHSA. Most buyers should prioritize the FHSA to capture the $8,000 annual room, then use the RRSP HBP to bridge the remaining gap. You can find more details on these and other Federal home buying incentives to ensure you aren’t leaving money on the table.

Short-Term Investment Options for Your Deposit

As you approach your purchase date, the safety of your principal becomes more important than high returns. While the stock market is tempting, a sudden correction could delay your home purchase by years. In 2026, High-Interest Savings Accounts (HISAs) and short-term GICs are the preferred choices for funds needed within twelve months. It’s also vital to maintain liquidity; when you find the right home in the Durham Region, you’ll often need to produce a deposit within 24 hours of an accepted offer. Ensure your funds are held in an account that allows for immediate electronic transfer or bank draft issuance without multi-day waiting periods.

The ‘Hidden’ Costs: Ontario Land Transfer Tax and Closing Fees

Securing your mortgage pre-approval is a major milestone, but your financial planning isn’t complete until you account for the costs that arise on closing day. These expenses typically range from 1.5% to 4% of the purchase price and must be paid in cash; they cannot be rolled into your mortgage. Understanding how to prepare financially to buy a home in ontario means looking beyond the deposit to the line items that your lawyer will present in the final statement of adjustments. From provincial taxes to title insurance, these figures require the same analytical rigour as your initial savings plan.

At Noble Real Estate, we believe that transparency is the best way to reduce the stress of homeownership. By identifying these costs early, you can ensure your transition into a new home is straightforward and successful. We treat your purchase with the same care a CPA applies to a financial audit, ensuring no “hidden” fee catches you off guard when you’re ready to collect your keys.

The Land Transfer Tax Breakdown

Ontario’s Land Transfer Tax (LTT) operates on a sliding scale. You pay 0.5% on the first $55,000, 1.0% on the portion between $55,001 and $250,000, 1.5% up to $400,000, and 2.0% on the remaining amount up to $2 million. For a home at the March 2026 Ontario average price of $749,200, the LTT would be approximately $11,459. One of the greatest financial advantages of buying in Uxbridge or the surrounding Durham Region is the absence of a municipal land transfer tax. Unlike buyers in the City of Toronto, who pay a second tax of equal value, our local clients keep thousands of dollars in their pockets.

First-time home buyers can access a provincial rebate of up to $4,000. This effectively offsets the full tax for homes valued at $368,000 or less and provides a welcome reduction for more expensive properties. Your lawyer typically applies for this rebate during the closing phase, so you won’t need to wait for a tax refund check. It’s a simple process that helps make homeownership more achievable for those entering the market.

Beyond the Purchase Price: Day One Expenses

Title insurance is a critical, one-time expense that protects you against mortgage fraud, zoning non-compliance, and existing liens on the property. It’s a non-negotiable for most lenders and provides vital protection for you as the owner. You also need to budget for legal fees, which generally fall between $1,500 and $2,500 depending on the complexity of the transaction. These professionals handle the title search and ensure the deed is registered correctly in your name.

Be prepared for “adjustments” on closing day. If the seller has already paid the property taxes in Uxbridge for the full year, you’ll need to reimburse them for the portion of the year you will own the home. The same applies to utilities or pre-filled fuel tanks. We recommend maintaining a dedicated ‘closing cost fund’ separate from your down payment. This ensures that when moving day arrives, every detail is handled with the precision and care it deserves.

Navigating the Mortgage Roadmap: Pre-Approval to Closing

Securing a mortgage in 2026 is a process that demands both early preparation and ongoing discipline. While the previous sections focused on saving and debt ratios, the mortgage roadmap is where those efforts are verified by a lender. Learning how to prepare financially to buy a home in ontario requires a clear understanding of the difference between a casual pre-qualification and a formal pre-approval. A pre-qualification is merely a surface-level estimate based on unverified data, whereas a formal pre-approval involves a rigorous review of your credit history and income, providing a specific price range and a rate hold that protects you from market fluctuations.

To move through this stage successfully, you must have your documentation ready for scrutiny. Lenders typically require your last two years of T4s, recent pay stubs, and a letter of employment confirming your status and salary. If you are receiving financial help from family, you will also need a signed gift letter stating that the funds are not a loan. Having these documents organized in advance ensures your application moves quickly when you find the right property. If you are just beginning your search, reviewing Buying a Home in Uxbridge: The Complete Guide can help you align your mortgage expectations with the local market reality.

Passing the Stress Test in 2026

The mortgage stress test remains a significant hurdle for many Ontario buyers. To pass, you must prove you can afford payments at a qualifying rate, which is currently the greater of your mortgage contract rate plus 2% or the floor rate of 5.25%. This regulation ensures that homeowners can still manage their debt if interest rates rise in the future. One effective way to boost your borrowing power before applying is through debt consolidation. By paying off or merging high-interest credit cards into a lower-interest personal loan, you improve your debt-service ratios and present a lower risk to the bank.

You also have choices in how you secure your financing. While a big bank offers the convenience of an existing relationship, a mortgage broker can shop multiple lenders to find the most competitive terms for your specific situation. Regardless of the path you choose, the goal is to secure a commitment that fits your long-term financial strategy. For personalized guidance on how your financing impacts your search, our buyer representation services provide the expert oversight you need to navigate these decisions with confidence.

Finalizing the Approval

Once you have a pre-approval, your financial profile must remain frozen until the day you close. A common mistake is making a large purchase, such as a new car or expensive furniture on credit, during the period between the offer and the closing date. These actions change your debt-to-income ratios and can lead a lender to revoke your approval at the last minute. The final hurdle is the appraisal. The lender will send a professional to verify that the home’s value matches the purchase price, ensuring the property is sufficient collateral for the loan. By maintaining a stable financial profile and choosing a home with sound investment potential, you ensure a stress-free transition to homeownership.

The Noble Approach: Financial Rigour Meets Local Real Estate

Mastering how to prepare financially to buy a home in ontario is a significant achievement, but the final step is ensuring that your financial preparation translates into a sound long-term investment. At Noble Real Estate, we believe that real estate is more than a transaction; it’s a strategic asset in your financial portfolio. This is where “The Noble Approach” provides a unique advantage. By blending professional buyer representation with a deep background in finance as a CPA and CA, we offer a level of analytical rigour that goes far beyond the standard home tour.

We help you move from the mindset of simply “buying a house” to “managing a real estate investment.” In a market like 2026, where interest rates and inventory levels require careful navigation, having an advisor who understands the underlying numbers is critical. Whether you’re looking at a heritage home in Uxbridge or a modern build in Pickering, we look at the historical appreciation data, local tax trends, and potential maintenance liabilities. This ensures your purchase supports your overall financial health and long-term goals.

The Advantage of Analytical Expertise

Choosing the right partner for this journey is about finding a fit that prioritizes your peace of mind and financial security. When Choosing Real Estate Agents Near You, consider how an advisor evaluates a property’s future value. In a fluctuating market, we don’t just look at what a home is worth today. We evaluate the long-term ROI of different Durham Region neighbourhoods, helping you identify areas with strong growth potential and resilient infrastructure. This data-driven perspective ensures you aren’t just winning a bidding war, but making a choice that benefits your family for years to come.

Next Steps: Starting Your Journey

The path to homeownership in Ontario can feel complex, but it doesn’t have to be stressful. Your next step is to align your verified financial readiness with the current opportunities in the market. We invite you to book a discovery call for a tailored financial readiness assessment. This isn’t a high-pressure sales pitch; it’s a strategic conversation to define your goals and build a clear roadmap for your search.

You don’t have to navigate the Ontario market alone. With the right guidance and a commitment to your success, we can make your transition to a new home straightforward, enjoyable, and financially rewarding. Redefine your expectations of what a real estate service can be and step into your new home with the confidence that every detail has been handled with the utmost care.

Your Path to a Confident Home Purchase

Understanding how to prepare financially to buy a home in ontario involves more than just hitting a savings target. It’s about mastering the 39/44 debt-service rule and maximizing every tax incentive available to you in 2026. By prioritizing accounts like the FHSA and accounting for provincial land transfer taxes early, you transform a complex transaction into a manageable investment. You’ve done the research; now it’s time to apply that knowledge to your specific goals in Uxbridge and the Durham Region.

Led by Colin Noble, a consummate professional with a background as a CPA and CA, Noble Real Estate provides the analytical rigour and local expertise you need for a successful move. We specialize in making the transition to homeownership stress-free and straightforward through the Noble Approach. If you’re ready to redefine your real estate expectations, Book a Financial Strategy Session with Noble Real Estate today. We’re here to ensure your journey is as rewarding as the destination itself. Your future home is within reach, and we look forward to helping you secure it with confidence.

Frequently Asked Questions

How much money should I save for a down payment in Ontario?

The minimum down payment depends on the purchase price of the home. For properties up to $500,000, you need 5%. For the portion between $500,000 and $999,999, you must provide 10%, and any home priced at $1 million or more requires a full 20% down payment. For a home at the March 2026 average price of $749,200, your minimum down payment would be approximately $49,920.

What is the First-Time Home Buyer Land Transfer Tax Rebate in 2026?

In 2026, the Ontario provincial land transfer tax rebate for first-time buyers remains capped at a maximum of $4,000. This amount fully offsets the tax for homes priced at $368,000 or less. For homes above this price point, you’ll pay the remaining balance. This rebate is a key factor when calculating how to prepare financially to buy a home in ontario, as it reduces your immediate cash requirements on closing day.

Can I use my RRSP for a down payment if I’m not a first-time buyer?

You can use the Home Buyers’ Plan (HBP) again if you meet the four-year “non-homeowner” replacement rule. This means you haven’t occupied a home that you or your current spouse owned in the last four years. If you qualify, the 2026 withdrawal limit is $60,000 per person. This tax-free withdrawal must be repaid to your RRSP over a 15-year period starting the second year after your withdrawal.

How does the mortgage stress test work for Ontario buyers?

The stress test determines your borrowing limit by seeing if you can handle higher interest rates. Lenders calculate your debt ratios using a qualifying rate, which is either your actual mortgage contract rate plus 2% or the floor rate of 5.25%, whichever is higher. This ensures you can maintain your payments even if market conditions change. It’s a vital step in the Noble Approach to ensure your investment remains sustainable.

What are the average closing costs in the Durham Region?

You should budget between 1.5% and 4% of the home’s purchase price for closing costs. In the Durham Region, your primary expenses will be the provincial land transfer tax, legal fees, and title insurance. One significant advantage of buying in areas like Uxbridge is that you avoid the additional municipal land transfer tax found in Toronto, which can save you thousands of dollars in upfront cash.

Is the First Home Savings Account (FHSA) better than a TFSA for home savings?

The FHSA is generally the superior tool for home savings because it offers a double tax advantage. Contributions are tax-deductible, which lowers your annual income tax bill, and qualifying withdrawals for your down payment are tax-free. While a TFSA offers tax-free growth, it doesn’t provide the initial tax deduction. Maximizing your $8,000 annual FHSA limit is a highly effective way to accelerate your savings for an Ontario home.

What happens if my mortgage pre-approval expires before I find a home?

Most pre-approvals are valid for 90 to 120 days. If yours expires, you’ll need to provide your lender with updated financial documents, such as recent pay stubs and bank statements, to renew it. It’s important to know that if interest rates have risen or your credit score has changed during that time, your new pre-approval amount might be lower than the original one.

Do I need a 20% down payment to avoid mortgage insurance in Canada?

Yes, a down payment of at least 20% is required to avoid paying CMHC mortgage loan insurance premiums. If you put down between 5% and 19.99%, the insurance premium is added to your mortgage balance, increasing your total debt. However, for any home priced over $1 million, a 20% down payment is a legal requirement in Canada, meaning you won’t have the option for an insured mortgage at that price point.