Looking For More Great Content?

Get even more informative Toronto real estate news sent directly to your inbox by signing up for my newsletter here. All it takes is a few easy clicks.

The Hidden Costs of Buying a Home in Ontario: A 2026 Financial Guide

03/24/26 Uncategorized

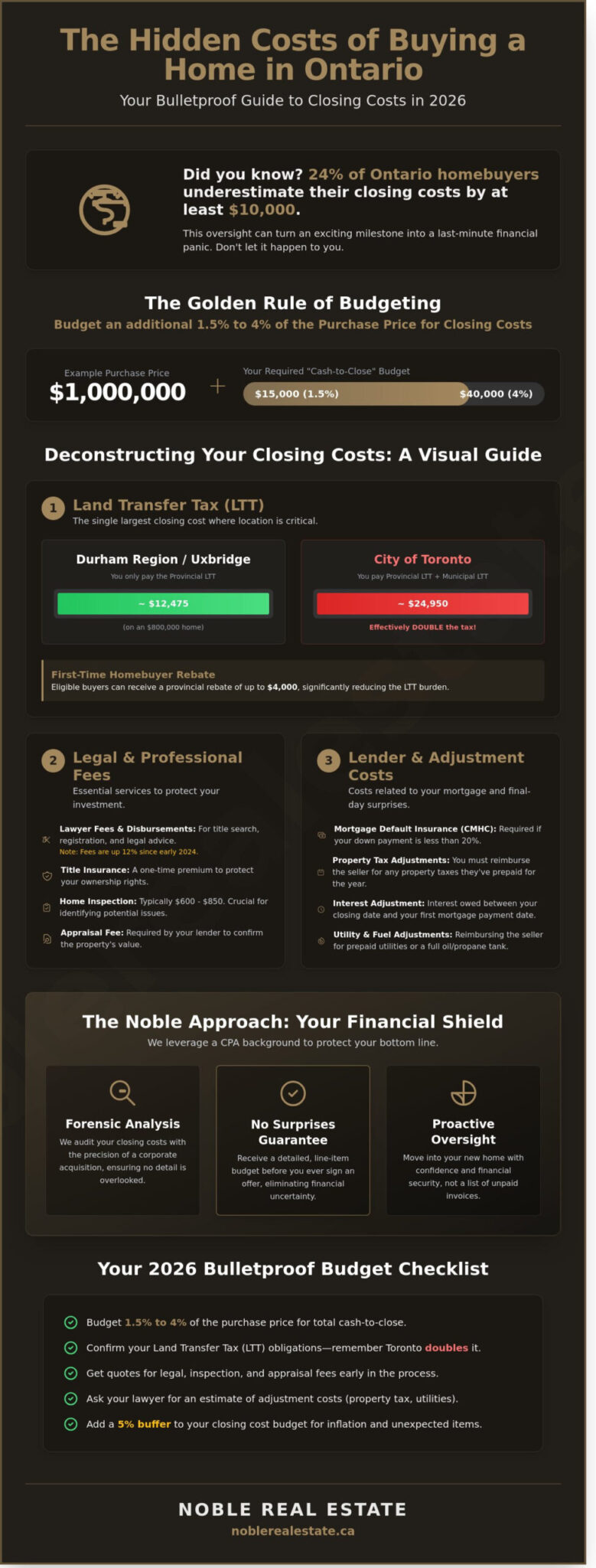

What if I told you that 24% of Ontario homebuyers underestimate their closing costs by at least C$10,000? Failing to account for the hidden costs of buying a home in Ontario can leave you facing a massive, unexpected bill just hours before you get your keys. Buying a home in Ontario’s 2026 market often feels like a high-stakes puzzle where the pieces keep moving. You’ve likely spent months saving for that down payment, only to feel a sense of anxiety when hearing whispers about double land transfer taxes and legal disbursements. It’s a common fear, but it doesn’t have to be your experience.

I’ll show you how to apply a professional financial lens to your purchase so you can move from confusion to absolute certainty. You’ll discover the exact line items that comprise your total cash-to-close requirement, including the specific provincial and municipal rules that often catch buyers off guard. We’ll break down every expense from title insurance to adjustment costs. This guide ensures your budget is bulletproof before you sign on the dotted line, allowing you to embrace The Noble Approach to a stress-free closing.

Key Takeaways

- Learn why budgeting an additional 1.5% to 4% of your purchase price is essential to cover the total “cash-to-close” requirement beyond the sticker price.

- Understand the financial impact of the hidden costs of buying a home in Ontario, from Land Transfer Tax to the long-term implications of CMHC insurance premiums.

- Identify specific regional expenses for Durham Region and Uxbridge, including the necessary inspections for rural properties that often catch buyers off guard.

- Discover how “The Noble Approach” leverages a CPA/CA background to audit your closing costs and protect your bottom line through proactive financial oversight.

Beyond the Sticker Price: Defining ‘Hidden’ Costs in Ontario (2026)

When you browse listings in Ontario, it’s easy to focus solely on the C$850,000 or C$1.2 million figure on the screen. That number is just the beginning of your financial commitment. A successful purchase requires distinguishing between the agreed-upon purchase price and the total cash-to-close requirement. Failing to account for the hidden costs of buying a home in ontario can turn an exciting milestone into a source of immense stress. You shouldn’t have to scramble for funds while you’re trying to pack boxes.

Industry standards suggest budgeting between 1.5% and 4% of the purchase price for these additional expenses. On a C$1,000,000 property, that equates to C$15,000 to C$40,000 in liquid cash. The psychological impact of an unexpected C$5,000 bill on closing day is profound. It shifts the experience from one of celebration to one of panic. My background as a CPA allows me to apply a rigorous, analytical lens to your transaction. This CPA-led approach, known as The Noble Approach, eliminates uncertainty by providing a detailed line-item breakdown before you ever sign an offer. You deserve to move into your new home with confidence, not a list of unpaid invoices.

By treating your home purchase like a corporate acquisition, we look at the hidden costs of buying a home in ontario through a forensic lens. We analyze property tax adjustments, which are often overlooked. If a seller has prepaid their taxes for the year, you’ll owe them a pro-rated amount on closing. On a C$6,000 annual tax bill, this could easily be a C$3,000 surprise if you close mid-year. We also account for:

- Title insurance premiums to protect your ownership.

- Appraisal fees required by your lender.

- Provincial and municipal land transfer taxes.

- Pro-rated utility and fuel tank refills.

What Exactly Are Closing Costs?

Closing costs are one-time fees paid at the conclusion of your real estate transaction. These are distinct from your down payment and include mortgage-related costs, such as appraisal fees, and legal or tax obligations like the Ontario Land Transfer Tax. Gaining a foundational level of understanding closing costs helps you anticipate where every dollar goes. Cash-to-close is the liquid capital needed on the final day of the sale.

The 2026 Economic Context for Ontario Buyers

In 2026, interest rates remain a primary driver of borrowing costs, directly affecting interest adjustments before your first mortgage payment. Inflation has also pushed service fees higher. Legal fees for a standard residential closing have increased by 12% since early 2024, and home inspections now average C$600 to C$850. Budgeting for a 5% buffer is the safest strategy in the current market to ensure your financial foundation remains secure.

The Big Three: Taxes, Insurance, and Legal Obligations

Preparation is the hallmark of a successful real estate journey. When you’re calculating your budget, the purchase price is just the starting point. Several mandatory expenses wait at the finish line, often catching buyers off guard. These hidden costs of buying a home in Ontario can total between 1.5% and 4% of your total purchase price. At Noble Real Estate, we believe in a “no surprises” philosophy, ensuring you have a clear financial roadmap long before closing day.

Ontario Land Transfer Tax vs. Toronto Municipal Tax

The Ontario Land Transfer Tax (LTT) represents the largest single closing cost for most buyers. In 2026, the provincial tax remains a tiered calculation. You’ll pay 0.5% on the first $55,000, 1.0% on the amount up to $250,000, 1.5% up to $400,000, and 2.0% on the remaining balance up to $2 million. For a $800,000 home, this amounts to roughly $12,475. If you’re a first-time homebuyer, you’re eligible for a provincial rebate of up to $4,000, which significantly offsets this burden.

Location matters immensely here. If you’re looking at property in Uxbridge or anywhere else in the Durham Region, you’ll save thousands compared to Toronto buyers. Residents in the 416 area code must pay an additional Municipal Land Transfer Tax that effectively doubles the tax bill. By staying in the surrounding communities, you avoid this secondary tax entirely. This distinction is a key part of The Noble Approach to finding value in the local market.

Mortgage Default Insurance (CMHC)

Many buyers opt for a down payment of less than 20%, which requires mortgage default insurance through providers like the CMHC. While the insurance premium itself is usually rolled into your monthly mortgage payments, the tax on that premium is not. In Ontario, you must pay an 8% Provincial Sales Tax (PST) on the CMHC premium upfront at the lawyer’s office. This is one of the most frequent hidden costs of buying a home in Ontario that buyers overlook.

Consider an $800,000 home with a 10% down payment of $80,000. Your mortgage amount is $720,000, and the current 2026 CMHC premium rate for this bracket is 3.10%, totaling $22,320. While that $22,320 is added to your loan, the 8% PST on that amount, $1,785.60, must be paid in cash on closing day. You can find more details on these upfront requirements in the Government of Canada’s home buying guide.

Legal Disbursements and Fees

Your real estate lawyer does more than just witness your signature. They’re responsible for the complex transfer of title and ensuring the property is free of liens or work orders. A standard legal bill in 2026 typically ranges from $1,500 to $2,500. This is split between the lawyer’s professional fee and “disbursements,” which are out-of-pocket costs the lawyer pays on your behalf for things like title searches, software transaction fees, and courier charges.

Title insurance is a critical component of this legal package. While technically optional, most lenders require it, and it’s a non-negotiable for smart buyers. For a one-time fee of approximately $400 to $900, it protects you against title fraud, existing work orders, or survey errors. It’s a small price for the peace of mind that your largest investment is legally secure from future litigation or ownership disputes.

The Durham Region Difference: Local Costs You Won’t Find in Toronto

Moving your search from the 416 to the Durham Region offers a breath of fresh air and more square footage, but it also introduces a new set of financial variables. While the purchase price might look more attractive, the hidden costs of buying a home in ontario often shift when you cross the Scarborough border. In Uxbridge or Scugog, you aren’t just buying a house; you’re often buying a self-sustained utility system. The Noble Approach involves looking beyond the list price to ensure your transition to the country doesn’t come with an unexpected bill.

One of the most immediate shocks for Toronto buyers is the property tax discrepancy. While Toronto benefits from a dense population that keeps residential tax rates around 0.66%, Durham municipalities like Whitby or Oshawa often see rates between 1.10% and 1.15%. On a C$900,000 property, this translates to an extra C$4,400 every year. Properly calculating your closing costs when buying a home must include these localized carry costs to ensure your monthly budget remains sustainable.

Environmental protections also play a massive role in Durham real estate. If your dream home sits near the Oak Ridges Moraine or within the jurisdiction of the Central Lake Ontario Conservation Authority (CLOCA), future renovations face strict scrutiny. A simple deck or a garage addition might require a conservation permit costing anywhere from C$600 to C$3,000, plus the cost of professional environmental impact studies. These are mandatory steps to protect our local ecosystem, but they are expenses city dwellers rarely encounter.

Specialized Inspections for Uxbridge Homes

Rural living requires a specialized toolkit for due diligence. If you’re eyeing a charming property in Uxbridge, a standard home inspection isn’t enough. You must budget C$500 to C$1,500 for specialized testing of private systems. A Wood Energy Technology Transfer (WETT) inspection, costing roughly C$250, is non-negotiable for homes with wood-burning stoves to satisfy insurance requirements. Additionally, you’ll need a flow rate test to ensure the well provides at least 3 to 5 gallons per minute and a potability test to confirm the water is safe for your family. Don’t skip the septic camera inspection; a failed leaching bed can lead to a C$20,000 replacement cost that no buyer wants to inherit.

Development Charges and New Build HST

The growth in Durham’s northern communities has led to an influx of new construction, which carries its own set of hidden costs of buying a home in ontario. When buying new, the 13% HST is often included in the sticker price if you intend to live there, but investors must pay this upfront and apply for a rebate later. You’ll also encounter Tarion warranty enrollment fees, which range from C$1,000 to C$1,800 for homes in the C$800,000 to C$1,000,000 range. Finally, always check the “builder’s adjustments” in your contract. In rapidly expanding areas, development levies for new schools or parks can be capped or uncapped; an uncapped levy could surprise you with a C$5,000 to C$10,000 bill on closing day.

The Noble Financial Checklist: Budgeting for the ‘Unseen’

Closing day is a milestone. It’s the moment the keys finally change hands and your vision for the future takes shape. However, the final number on your lawyer’s ledger often differs from your initial purchase price because of credits and debits known as adjustments. At Noble Real Estate, we believe that uncovering the hidden costs of buying a home in ontario requires an analytical eye; the same rigour I applied during my years as a CPA and CA. You shouldn’t be surprised by the “bottom line” when you sit down to sign your final documents.

Mastering the Statement of Adjustments

The Statement of Adjustments is the lawyer’s final tally of who owes what. It ensures the seller is reimbursed for any expenses they’ve prepaid beyond the closing date. For example, if the seller paid the full C$4,800 annual property tax bill in January and you close on November 1st, you’ll owe them a pro-rated credit for the final two months. This process also applies to fuel tanks. If the home uses oil or propane, the seller will often fill the tank before closing, and you’ll be charged for the value of the remaining fuel. A final walk-through 24 hours before closing is essential to ensure the property’s condition matches the agreement, preventing last-minute adjustment disputes.

The ‘Day One’ Maintenance Fund

Your financial obligations don’t end when the moving truck pulls away. Immediate security and privacy upgrades are essential for peace of mind. We recommend budgeting C$300 to C$600 to have a locksmith change all exterior locks and reprogram garage codes immediately. Another frequently forgotten expense is window coverings. Outfitting a standard detached home with basic blinds or shades can easily cost C$2,000 to C$5,000. To protect your investment, The Noble Approach suggests setting aside 1% of the home’s purchase price as an emergency fund. On a C$950,000 home, having C$9,500 liquid ensures you can handle a failed sumppump or a furnace hiccup without financial strain.

Managing these details is a vital part of managing the hidden costs of buying a home in ontario effectively. If you want a partner who looks at your purchase through a financial and community-focused lens, connect with Noble Real Estate today to start your journey.

Moving and Utility Setup Fees

Logistics in 2026 require early planning and a realistic budget. In the Durham Region, professional moving companies currently charge approximately C$185 to C$210 per hour for a three-person crew and a five-tonne truck. A local move for a three-bedroom house typically spans 8 to 10 hours, totaling roughly C$1,850 before HST and gratuities. Beyond the physical move, you’ll encounter various administrative fees:

- Utility Hook-ups: New accounts for hydro, water, and natural gas often carry setup fees ranging from C$35 to C$50 each.

- Security Deposits: If you’re a first-time utility customer, some providers may require a deposit of C$200 to C$300 which is held against your first year of billing.

- The Cost of Time: Don’t forget to budget for two or three days of unpaid time off work to coordinate deliveries, utility technicians, and the move itself.

Our goal is to make this transition stress-free and straightforward. By accounting for these “unseen” numbers early in the process, you ensure that your first night in your new Ontario home is spent celebrating your success rather than worrying about the ledger.

Stress-Free Closing: How the Noble Approach Protects Your Bottom Line

Closing day shouldn’t feel like a high-stakes gamble. While the previous sections of this guide detailed the various hidden costs of buying a home in ontario, the final step in your journey is ensuring those numbers are managed with absolute precision. We don’t just hope for the best; we audit the entire process to ensure you aren’t paying a cent more than necessary.

The Financial Rigor of Colin Noble

Colin Noble brings a level of analytical depth that is rare in the real estate industry. With a professional background as a CPA and CA, he views every transaction through a lens of financial accountability and risk mitigation. This rigor is essential when reviewing your Statement of Adjustments. Banks and legal offices are run by humans, and humans occasionally make errors. A 0.1% miscalculation on a C$900,000 mortgage or a botched property tax adjustment can result in unexpected out-of-pocket expenses. By choosing The Noble Approach: Why Our Listings Sell, you gain a partner who understands the complex math behind the deal, ensuring your bank documents are accurate and your interests are protected.

Online calculators often fail because they rely on broad provincial averages. In Ontario, closing costs typically range from 1.5% to 4% of the purchase price. On a C$1,200,000 home in Uxbridge, that represents a massive variance of C$30,000. We replace these generic guesses with a personalized financial strategy. Our team initiates proactive communication with your lender and lawyer at least 14 days before your closing date. This specific timeline allows us to identify and resolve discrepancies before they become urgent problems, such as:

- Miscalculated Land Transfer Tax rebates for first-time buyers.

- Incorrectly prorated property tax adjustments between buyer and seller.

- Unexpected legal disbursements that exceed your initial estimates.

- Discrepancies in title insurance premiums based on specific property risks.

Your Path to a Successful Purchase

A formal Buyer Representation agreement is the foundation of this protection. It commits our full resources to your financial well-being, from the initial search to the moment you turn the key. We act as the central hub of your purchase, coordinating directly with your financial advisor and mortgage broker to ensure funds are ready and all conditions are met well ahead of schedule. This end-to-end approach removes the friction and anxiety often associated with the hidden costs of buying a home in ontario. You deserve a transition into your new home that is as rewarding as the destination itself. Start Your Uxbridge Home Search With Us Today and experience a higher, more principled standard of real estate service that redefines your expectations.

Secure Your Financial Future in the Ontario Housing Market

Navigating the 2026 real estate landscape requires more than just a down payment. You need to account for the 1.5% to 4% of the purchase price typically required for closing fees. These hidden costs of buying a home in ontario, such as provincial land transfer taxes and legal disbursements, can impact your bottom line if you aren’t prepared. By choosing the Durham Region over Toronto, you avoid the municipal land transfer tax, keeping more capital in your pocket for your new life in Uxbridge. It’s a significant financial advantage that many first-time buyers overlook.

Led by Colin Noble, a CPA and CA, our team brings analytical precision to your home search. We transform complex financial data into a clear, supportive roadmap for your move. This expert local knowledge ensures you won’t face any unwelcome surprises on closing day. We believe the process of buying a home should be as rewarding as the day you get your keys. Our end-to-end approach reduces stress and redefines what you should expect from a real estate partner. You don’t have to manage these variables alone.

Ready to find your Uxbridge home? Let the Noble Approach guide you.

It’s time to move forward with a plan that protects your investment and your peace of mind.

Frequently Asked Questions

How much should I budget for closing costs in Ontario?

You should budget between 1.5% and 4% of your home’s purchase price to cover the hidden costs of buying a home in Ontario. For a C$800,000 property, this means setting aside C$12,000 to C$32,000 in liquid cash. These funds cover taxes, legal fees, and administrative expenses that your mortgage won’t include. Having this liquidity ensures your closing day remains stress-free and predictable for your family.

Do first-time homebuyers get a break on Land Transfer Tax?

Eligible first-time homebuyers receive a provincial Land Transfer Tax refund of up to C$4,000. This credit applies to the full or partial amount of the tax for homes priced up to C$368,000. If your home costs more, you’ll pay the difference. To qualify, you must be a Canadian citizen or permanent resident and at least 18 years old. This incentive helps reduce the immediate financial burden of your first purchase.

What is the difference between provincial and municipal Land Transfer Tax?

Provincial Land Transfer Tax applies to every property purchase in Ontario, while the Municipal Land Transfer Tax only applies to homes within the City of Toronto. If you’re buying in Ontario cities like Uxbridge or Ottawa, you only pay the provincial portion. Toronto buyers essentially pay double the tax. This can add C$15,000 or more to the total hidden costs of buying a home in Ontario depending on the price.

Is a home inspection a mandatory cost in Ontario?

A home inspection isn’t legally mandatory in Ontario, but it’s a critical step for protecting your investment. Most buyers spend between C$400 and C$600 for a professional assessment of the property’s condition. Skipping this step might save money upfront, but it exposes you to thousands in potential repair costs later. We recommend including an inspection condition in your offer to ensure the property’s structural integrity and your own peace of mind.

What are ‘adjustments’ on a real estate closing?

Adjustments are payments made to the seller for costs they’ve already paid that extend past the closing date. These typically include property taxes, fuel oil, or prepaid utility bills. If a seller paid the full year of property taxes in January and you buy in July, you’ll owe them for the remaining six months. Your lawyer calculates these figures to ensure a fair transfer of financial responsibility between both parties.

Do I have to pay HST when I buy a house in Ontario?

You only pay the 13% Harmonized Sales Tax (HST) on the purchase of brand-new homes or properties that underwent substantial renovations. Resale homes are generally exempt from this tax. If you buy a new build for C$900,000, the HST is often included in the sticker price, but you should confirm this with your builder to avoid a C$117,000 surprise. This distinction is vital for your total budget planning.

How much are legal fees for buying a house in 2026?

Expect to pay between C$1,500 and C$2,500 for legal fees and disbursements by 2026. This estimate covers your lawyer’s time, title insurance, and various administrative search fees. While base fees might sit around C$1,000, disbursements for government registrations add several hundred dollars to the final bill. The Noble Approach ensures you have a detailed breakdown of these costs well before your closing date to avoid any last-minute confusion.

Can I add my closing costs to my mortgage?

You can’t add your closing costs to your mortgage; these must be paid as liquid cash at the time of closing. Lenders require proof that you have these funds available in addition to your down payment. While you can’t roll them into the loan, some buyers negotiate a cash back mortgage or use a line of credit, though these options carry higher interest rates. Planning for this cash outlay is essential for success.