Looking For More Great Content?

Get even more informative Toronto real estate news sent directly to your inbox by signing up for my newsletter here. All it takes is a few easy clicks.

The Mortgage Pre-Approval Process in Canada: A 2026 Strategic Guide for Homebuyers

03/16/26 Uncategorized

What if your mortgage pre-approval was more than just a bank letter, but actually the sharpest negotiating tool in your pocket when bidding on a home in Uxbridge? Most buyers in the Durham Region feel a heavy sense of dread when they think about the OSFI stress test, which currently requires you to qualify at a rate 2% higher than your actual contract rate. It’s natural to feel anxious as home prices in Uxbridge rose by 4.2% in the first quarter of 2026 alone. You likely believe that the mortgage pre-approval process canada requires is a hurdle designed to limit your options, but we see it differently.

Through The Noble Approach, we’ll show you that this step is actually your greatest advantage. You’ll learn exactly how to secure that “golden ticket” and use your financial status to outmaneuver other bidders in a competitive market. This guide provides a clear, four-step roadmap to understanding your true purchasing power and entering the local market with the analytical rigour of a seasoned financial advisor. We’re going to demystify the paperwork and give you the confidence to start your house hunt today.

Key Takeaways

- Understand why a formal pre-approval is your “Golden Ticket” in the 2026 Durham Region market, providing a level of financial certainty that simple estimates cannot match.

- Navigate the mortgage pre-approval process canada through a structured five-step journey designed to transition you from initial document gathering to a fully verified status.

- Discover how to optimize your down payment and maximize your purchasing power by strategically utilizing Canadian tools like the FHSA and RRSP Home Buyers’ Plan.

- Learn “The Noble Approach” to leveraging your pre-approved status as a powerful negotiating tool to secure lower purchase prices and more competitive contract terms.

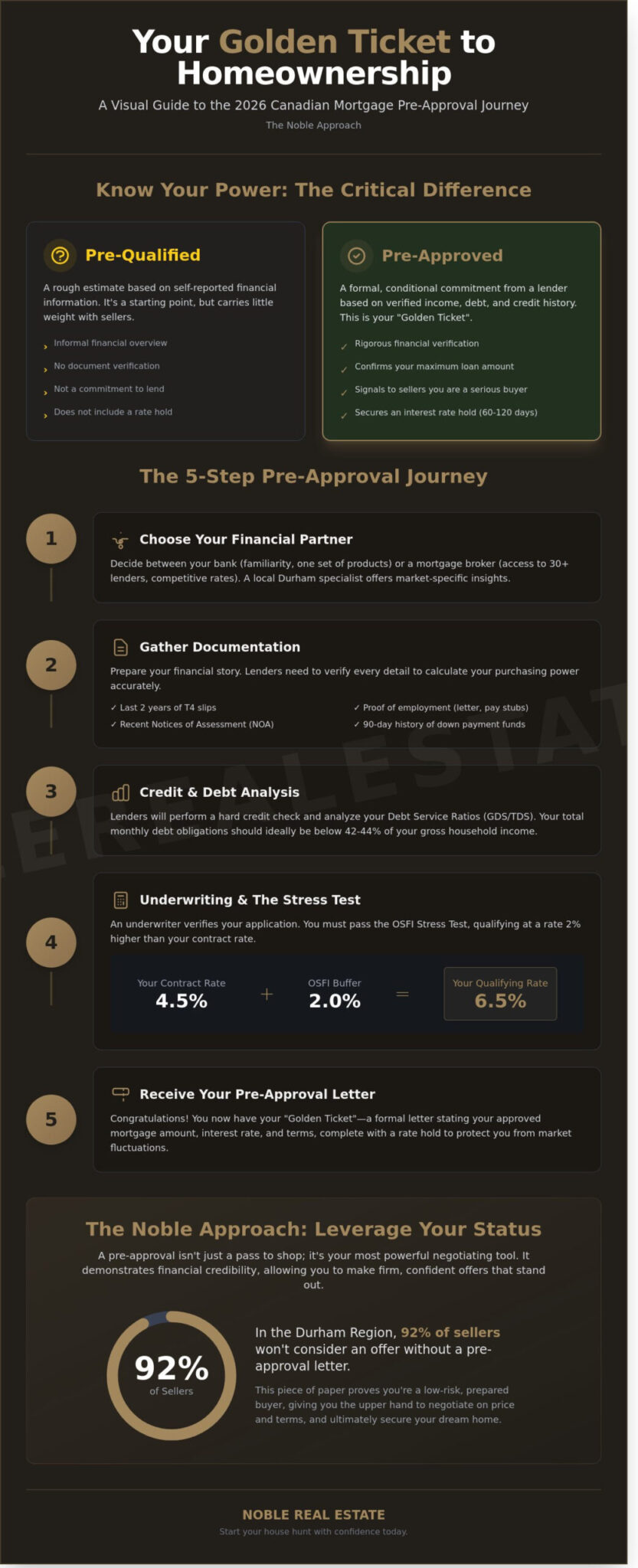

- Identify the critical differences between being pre-qualified and pre-approved to ensure your offers are presented with the analytical rigour and credibility sellers demand.

What is the Mortgage Pre-Approval Process in Canada?

The mortgage pre-approval process canada is the essential first step in your home-buying journey. It’s a formal statement from a Canadian lender that specifies the maximum loan amount you’re eligible to receive based on a deep dive into your financial health. This isn’t just a casual estimate; it’s a rigorous verification of your income, credit score, and debt-to-income ratios. In the 2026 Canadian real estate market, where inventory remains tight and competition is fierce, this document has become the “Golden Ticket” for serious buyers. Without it, you’re essentially window shopping without a wallet.

A critical distinction to understand is the difference between a verbal “OK” from a bank teller and a formal pre-approval letter. A verbal nod carries no weight in a legal offer. A formal letter, however, signifies that a lender has reviewed your T4 slips, pay stubs, and credit history. Understanding What is a Mortgage Pre-Approval helps you realize that this document serves as a conditional commitment. It also provides a vital safety net: a rate hold. Most Canadian lenders will lock in your quoted interest rate for 60, 90, or 120 days. If the Bank of Canada raises rates by 25 or 50 basis points while you’re house hunting, your lower rate remains protected, potentially saving you thousands of dollars over your mortgage term.

The Core Purpose: Budgeting and Confidence

The Noble Approach emphasizes starting your search with clarity rather than guesswork. Obtaining a pre-approval allows you to establish a firm price ceiling before you begin scrolling through MLS listings. This prevents the emotional exhaustion of falling in love with a C$1,200,000 property when your actual qualifying limit is C$950,000. In the Durham Region, local data from early 2026 shows that 92% of sellers in areas like Uxbridge and Pickering won’t even consider an offer that doesn’t include a pre-approval letter. It signals that you’re a prepared, low-risk buyer who can actually close the deal.

Understanding the 2026 Mortgage Stress Test

Even as we move through 2026, the federal mortgage stress test remains a primary hurdle for Canadian buyers. This regulation requires you to prove you can handle payments at a “qualifying rate,” which is usually 2% higher than your actual contract rate. If your lender offers you a 4.5% fixed rate, you must qualify as if the rate were 6.5%. This calculation directly impacts your Total Debt Service (TDS) ratio. Most lenders require your total monthly debt obligations, including the new mortgage, taxes, and heat, to stay below 42% of your gross household income. Knowing these numbers upfront ensures your home-buying experience stays stress-free and financially sustainable.

The 5 Essential Steps of the Canadian Pre-Approval Journey

Securing a home in the current market requires more than just a wish list; it demands a structured financial strategy. The mortgage pre-approval process canada involves five distinct stages that transform you from a browser into a serious, qualified buyer. This journey provides the clarity you need to shop with confidence, knowing exactly what the monthly carry will look like for your family. By following these steps, you eliminate the guesswork and position yourself as a preferred candidate in a competitive bidding environment.

Step 1: Choosing Between a Bank and a Mortgage Broker

Your first decision is determining who will represent your interests. Staying with your primary financial institution offers the comfort of an existing relationship, yet it often limits you to a single suite of products. Conversely, a mortgage broker acts as an intermediary with access to over 30 different lenders, including credit unions and monoline firms. This competition is vital for securing the best 2026 rates as market conditions evolve. The Noble Approach recommends partnering with a local Durham Region specialist who understands the unique nuances of the Uxbridge and Pickering markets. A seasoned professional with a background in finance can help you weigh these options through an analytical lens, ensuring your mortgage structure aligns with your long term wealth goals.

Steps 2 & 3: Documentation and Credit Health

Preparation is the antidote to stress during the financial deep dive. You’ll need to gather your last two years of T4 slips, recent Notices of Assessment (NOAs) from the CRA, and a 90-day history of your down payment funds. Lenders use these to calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. In most cases, your total debt obligations shouldn’t exceed 44% of your gross income. The Government of Canada provides detailed guidelines on the Canadian mortgage pre-approval process to ensure you meet these federal stress test requirements. Your credit score also dictates your interest rate tier; a score above 720 typically unlocks the most competitive pricing, while scores below 680 may require alternative lending solutions or higher premiums.

Once your documentation is submitted, the lender performs a formal review of your application. This results in a conditional commitment, which is a preliminary “yes” based on the data provided. It’s a powerful tool to have in hand when you’re ready to explore available listings in your preferred neighbourhood, as it proves to sellers that you have the financial backing to close the deal.

Step 5: Protecting Your Pre-Approval Status

Receiving your pre-approval letter is a significant milestone, but it isn’t a guarantee of final funding. Most Canadian lenders offer a rate hold that lasts between 90 and 120 days. If this period expires before you find a home, your promised rate may be subject to current market increases. You must maintain your financial profile exactly as it was during the initial application. Avoid financing a new C$60,000 vehicle or making large furniture purchases on credit; these new liabilities can shift your debt ratios and disqualify you instantly. Similarly, changing your employment status or moving from a salaried position to a contract role can invalidate your status. Stay consistent, keep your debt levels low, and communicate any potential life changes to your advisor immediately to keep your mortgage pre-approval process canada on track.

Pre-Qualified vs. Pre-Approved: Crucial Differences for Buyers

Understanding the distinction between these two terms is the difference between a successful closing and a heartbreaking deal collapse. A pre-qualification acts as a helpful starting point, but it’s essentially a surface-level estimate. You provide a lender with unverified details about your income and debt, and they offer a non-binding figure of what you might afford. It doesn’t involve a deep dive into your credit history or a review of your tax returns.

Step 4: Lender Review and Formal Pre-Approval

A formal pre-approval is a rigorous verification process. The lender performs a hard credit check and scrutinizes your T4s, pay stubs, and bank statements to confirm your financial standing. This step is a vital component of the mortgage pre-approval process canada because it results in a written commitment for a specific loan amount and interest rate, usually guaranteed for 90 to 120 days. According to the Financial Consumer Agency of Canada, this process helps you identify any obstacles in your credit report early, giving you time to resolve them before you start touring homes.

Relying on a pre-qualification during the 10-day financing condition period is a high-risk strategy. If the lender discovers undisclosed debt or inconsistent income during the final verification, they may deny the loan. This leads to a deal collapse, which can result in the loss of your deposit and potential legal action from the seller. From a seller’s perspective, a formal pre-approval letter is a powerful psychological tool. In competitive markets like Uxbridge, sellers often prioritize offers backed by a verified pre-approval because it minimizes the risk of the transaction falling through at the eleventh hour.

The Danger of the ‘Online Calculator’ Trap

Generic online tools are often too simplistic for the Canadian market. They frequently omit local property taxes, which can range from 0.5% to 1.5% of the home’s value depending on the municipality. These calculators also ignore the mortgage pre-approval process canada requirements regarding the Gross Debt Service (GDS) ratio. For instance, a monthly condo fee of C$350 or estimated heating costs of C$150 can reduce your borrowing power by more than C$45,000. The Noble Approach utilizes a professional CPA-led analysis to ensure every line item, from strata fees to closing costs, is accounted for before you make an offer.

When Pre-Approval Isn’t Final Approval

A pre-approval focuses on you, the borrower, but the final mortgage approval depends heavily on the property itself. Lenders include “conditions” in your pre-approval letter, such as a satisfactory property appraisal and a clean title search. If you offer C$850,000 for a home but the bank’s appraiser values it at C$810,000, the lender will only provide financing based on the lower number. You would then need to cover that C$40,000 gap out of pocket. We guide you through these scenarios by analyzing comparable sales data to ensure your offer aligns with current market valuations, keeping your journey stress-free and straightforward.

Actionable Guidance: Preparing for Your Mortgage Application

Success begins 180 days before you visit a lender. The Noble Approach emphasizes a proactive six-month financial cleanup to ensure your profile is pristine when lenders begin their scrutiny. Taking control of the mortgage pre-approval process canada involves a structured 180-day strategy. You should start by reviewing your credit report for errors; a 20-point boost in your score can sometimes lower your offered interest rate by 0.25%, saving you thousands over a five-year term.

Strategic saving is equally vital. You can now maximize your down payment using the Tax-Free First Home Savings Account (FHSA), which allows for C$8,000 in annual contributions up to a C$40,000 lifetime limit. Following the April 16, 2024, federal budget announcement, the RRSP Home Buyers’ Plan limit also increased to C$60,000. Utilizing these tools effectively reduces the principal you need to borrow, directly impacting your monthly cash flow.

Maximizing Your Borrowing Power

Your Total Debt Service (TDS) ratio is the primary metric lenders use to judge your file. To improve this, prioritize paying down high-interest debt like credit cards, which often carry rates of 19.99% or higher. If your income doesn’t quite meet the threshold for the home you want, a co-signer can provide the necessary lift. In the current market, roughly 25% of first-time buyers in Ontario utilize a co-signer to bridge the gap. Remember that reaching a 20% down payment is the “gold standard” because it eliminates the need for CMHC insurance premiums, which can add up to 4% to your total mortgage amount.

Durham Region Market Specifics

Uxbridge offers a unique lifestyle, but it requires specific financial planning. Property taxes in Uxbridge typically hover around 0.9% to 1.1% of the assessed value, a figure that must be factored into your qualifying ratios. Local lenders often provide an advantage here because they understand rural property nuances. If you’re looking at homes outside the town center, lenders will require specific tests for wells and septic systems. These aren’t just “nice to have” details; they’re mandatory requirements for mortgage approval on rural lots.

Closing costs are another area where buyers are often surprised. You should budget between 1.5% and 4% of the purchase price for these expenses. In Ontario, this includes the Land Transfer Tax, legal fees, and title insurance. For a C$900,000 home in Durham Region, you should have at least C$18,000 set aside in a liquid account to cover these transition costs comfortably. This structured preparation ensures the mortgage pre-approval process canada remains a source of confidence rather than stress.

To expedite the lender’s response, build a “Mortgage Ready” folder containing these essential documents:

- Income Verification: Your two most recent T4s and your Notice of Assessment (NOA) from the CRA.

- Employment Proof: A letter from your employer dated within the last 30 days and two recent pay stubs.

- Down Payment Evidence: Three months of bank statements showing the accumulation of funds.

- Property Details: For those with existing properties, your most recent mortgage statement and property tax bill.

Ready to start your journey with a partner who understands the numbers as well as the neighborhoods? Connect with Noble Real Estate today to receive a personalized assessment of your mortgage readiness.

The Noble Approach: Leveraging Your Pre-Approval to Win

Securing a pre-approval isn’t just a box to check; it’s a powerful tool in your negotiation arsenal. When you enter the Uxbridge market with a verified budget, you’re no longer just a “looker.” You’re a qualified buyer. This status allows us to negotiate from a position of strength. Sellers in Durham Region often prioritize certainty over the highest price tag. By showing that your mortgage pre-approval process canada is already complete, we signal to the listing agent that your offer is a sure thing.

One of the most effective ways we use this status is by shortening the financing condition period. While a standard offer might include a 5 to 7-day window to secure funds, a pre-approved buyer can often reduce this to 2 or 3 business days. In some cases, if the lender has already performed a full underwriting review of your documents, we can even discuss waiving the condition entirely to beat out multiple offers. This speed makes your proposal significantly more attractive to a seller who wants a quick, clean transaction.

Success relies on a seamless triad of communication. The Noble Approach ensures your Realtor, lawyer, and mortgage specialist are in constant contact. As a CPA and CA, I look at your purchase through a financial lens, ensuring that the math behind your closing costs, land transfer taxes, and down payment is flawless. This end-to-end oversight prevents the “closing day panic” that occurs when professionals work in silos. We aim for a transition that’s as quiet and professional as the Uxbridge countryside.

Strategic Offer Presentation

We present your financial strength without giving away your hand. It’s a delicate balance. We want the listing agent to know you’re fully qualified for the purchase price, but they don’t need to know your maximum ceiling. This redefines expectations; the seller sees a buyer who is prepared, serious, and respectful of the process. This level of readiness often leads to smoother inspections and more cooperative sellers during the final walk-through.

Consider a real-world example from October 2023. A client of mine was eyeing a property in Uxbridge listed at C$950,000. We faced a competing bid that was actually C$15,000 higher than ours. However, because my client had completed the mortgage pre-approval process canada and we could provide a letter of intent from the lender, the seller chose us. The other buyer had no proof of funds and requested a 10-day financing clause. The seller valued the C$950,000 “sure thing” over the C$965,000 “maybe.”

Your Next Steps Toward Homeownership

The journey to your new front door begins with a clear plan. Your first step is booking an initial consultation to review your current financial standing and long-term goals. We’ll look at your income, debts, and savings to build a realistic roadmap. This isn’t just about a number; it’s about making sure your home fits your lifestyle without creating financial strain.

Once your pre-approval is in hand, we immediately align your budget with our current Uxbridge home listings. We don’t waste time on properties that don’t fit your criteria or your bank’s requirements. The Noble Promise is simple: you’ll receive expert guidance from that very first calculation to the moment the final key turns in the lock. We’re here to make the complex feel straightforward and the stressful feel exciting.

Take the Lead in the 2026 Durham Region Market

Mastering the mortgage pre-approval process canada is your most strategic move before visiting a single open house. It transforms you from a casual browser into a serious contender by providing a locked-in interest rate and a verified C$ budget. This clarity is essential when navigating the competitive landscapes of Uxbridge and Durham Region. By distinguishing between a simple pre-qualification and a rigorous pre-approval, you ensure your offer stands out to sellers who value certainty in a fast-moving market.

My background as a CPA and CA provides you with an analytical edge that most agents can’t match. I use this financial expertise to ensure your investment is sound and your transition is seamless. We don’t just find houses; we secure your financial future through a proven, stress-free methodology. You deserve a partner who understands both the local community and the complex numbers behind every deal.

Your journey toward a new home should be as rewarding as the destination itself. Let’s make your 2026 real estate goals a reality with confidence and precision.

Frequently Asked Questions About Mortgage Pre-Approval

How long does the mortgage pre-approval process take in Canada?

The mortgage pre-approval process in Canada typically takes between 24 and 48 hours once you submit your full documentation package to a lender. This timeline can extend to five business days during peak spring markets or if your financial situation requires a more complex review by an underwriter. Having your tax returns and pay stubs ready ensures the journey remains stress-free and straightforward.

Does a mortgage pre-approval affect my credit score?

A mortgage pre-approval involves a hard credit inquiry, which typically results in a temporary decrease of five points to your credit score. However, credit bureaus like Equifax and TransUnion treat multiple inquiries for the same purpose within a 45-day window as a single event. This allows you to shop for the best rate without damaging your credit profile or long-term financial health.

How long is a mortgage pre-approval valid for in Ontario?

Most lenders in Ontario guarantee your pre-approved interest rate for a period of 90 to 120 days. This protection is vital because it shields you from market fluctuations while you browse listings. If you don’t find a home within this four-month window, you’ll need to provide updated income documents to renew the commitment and maintain your rate lock.

Can I get pre-approved for a mortgage if I am self-employed?

You can certainly get pre-approved as a self-employed borrower by providing your T1 General tax returns and Notices of Assessment for the last two years. Lenders typically average your net income from these 24 months to determine your borrowing capacity. The Noble Approach focuses on presenting your business’s financial health clearly to ensure lenders see the full value of your professional success.

What happens if interest rates drop after I am pre-approved?

If market interest rates drop by 0.25% or more after your pre-approval, your lender will typically adjust your rate downward to match the current offer. Your pre-approval acts as a rate ceiling, protecting you from increases while allowing you to benefit from any decreases before your closing date. This ensures you always secure the most competitive financial terms available in the 2026 market.

Is a mortgage pre-approval a guarantee that I will get the loan?

A pre-approval isn’t a 100% guarantee of funding because the final loan approval depends on a satisfactory property appraisal and your financial status remaining unchanged. If you change jobs or take on a C$40,000 car loan before closing, the lender may revoke the offer. It’s a critical step in the mortgage pre-approval process in Canada, but the final commitment only happens once a specific property is vetted.

Do I need a pre-approval before I start looking at houses in Uxbridge?

Obtaining a pre-approval before touring homes in Uxbridge is essential because it defines your exact budget and signals to sellers that you’re a qualified buyer. In competitive local markets, sellers often prioritize offers that include a pre-approval letter over those without financial backing. This preparation makes your home-buying journey more enjoyable and prevents the disappointment of falling in love with a property that sits outside your financial reach.

What documents are required for a Canadian mortgage pre-approval in 2026?

To secure a pre-approval in 2026, you must provide a valid government ID, your most recent T4 slips, and pay stubs from the last 30 days. You’ll also need to show proof of your down payment through three months of bank statements or a gift letter if receiving funds from family. These documents allow your advisor to conduct a thorough analysis, ensuring your path to homeownership is both transparent and successful.