Looking For More Great Content?

Get even more informative Toronto real estate news sent directly to your inbox by signing up for my newsletter here. All it takes is a few easy clicks.

First-Time Home Buyer Ontario Guide: Navigating the 2026 Market

05/2/26 Uncategorized

Did you know that a first time home buyer ontario in 2026 can now access over $180,000 in combined government tax rebates and incentives? While the high cost of living in the Durham Region often feels like a barrier, the current buyer’s market offers a rare window of opportunity for those with a sharp financial strategy. You likely feel the pressure of rising costs and the confusion of choosing between an FHSA or the new $60,000 RRSP withdrawal limit. These decisions shouldn’t be stressful; they should be the foundation of your future wealth.

This guide provides a clear financial roadmap to help you master the 2026 market with confidence and ease. We’ll explore how the 2.25% Bank of Canada policy rate impacts your budget, how to claim the maximum Ontario Enhanced HST Rebate, and why communities like Uxbridge, with an average price of $995,779, represent such strong value right now. By using a professional, analytical approach, you can eliminate the fear of hidden closing costs and secure your first home with total clarity. It’s time to redefine your expectations of what the home-buying journey can be.

Key Takeaways

- Define your eligibility for 2026 provincial and federal programs to ensure you capture every available rebate and incentive as a first time home buyer ontario.

- Navigate the financial advantages of the FHSA and the newly expanded RRSP Home Buyers’ Plan to build a more robust, tax-efficient down payment.

- Apply an analytical, CPA-led approach to your mortgage strategy to understand the critical difference between being pre-qualified and fully pre-approved.

- Identify high-value opportunities in the Durham Region and learn why the Uxbridge micro-market offers a unique blend of lifestyle and investment resilience.

- Follow “The Noble Approach” to the closing process, turning complex negotiations into a straightforward and successful transition to your new home.

Understanding the 2026 First-Time Home Buyer Landscape in Ontario

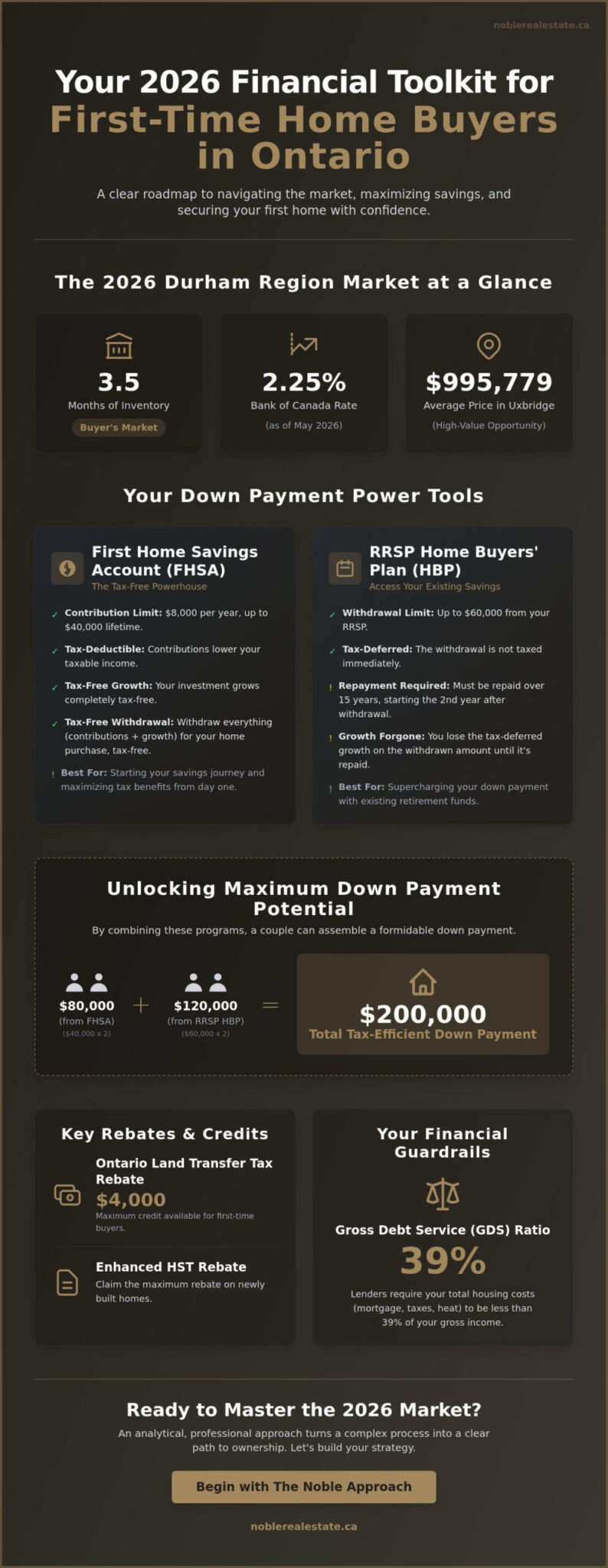

Ontario’s real estate market continues to prove its durability. In early 2026, we see a distinct shift in the Durham Region, which is currently classified as a buyer’s market with 3.5 months of inventory as of April 2026. This environment provides a unique opportunity for those ready to transition from a renter’s mindset to that of an asset owner. It’s a significant psychological leap. You’re moving away from viewing housing as a monthly expense and toward seeing it as a long term financial foundation. Making this move successfully requires “The Noble Approach,” which blends local expertise with the analytical rigor of a finance professional to navigate today’s inventory challenges.

Every first time home buyer ontario must start with a clear understanding of their financial position. With approximately 33% of Canadian mortgage holders expected to face higher payments by the end of 2026, entering the market with a structured plan is essential. We focus on making the complex straightforward, ensuring you feel confident rather than overwhelmed by the sheer volume of market data.

Are You Eligible? The First-Time Buyer Criteria

Defining your status is the primary step toward unlocking significant government incentives. A First-time buyer isn’t always someone who has never owned property. Under the “four-year rule,” you may re-qualify if you haven’t occupied a home owned by you or your current spouse in the four years preceding your purchase. This rule opens doors for many who are returning to the market after a period of renting. To claim the $4,000 Ontario Land Transfer Tax rebate, you must be a Canadian citizen or permanent resident and occupy the home as your principal residence within nine months of the transfer.

The Financial Reality Check: Gross Debt Service (GDS) Ratios

Financial readiness starts with the 39% rule. Lenders use the Gross Debt Service (GDS) ratio to ensure your housing costs, including mortgage, taxes, and heating, don’t exceed 39% of your gross monthly income. As of May 2026, the Bank of Canada policy rate sits at 2.25%, with the lenders’ prime rate at 4.45%. These figures directly dictate your purchasing power. A stress-free experience begins with an honest look at your debt load and a professional assessment of how these rates impact your monthly cash flow. We believe that a successful purchase isn’t just about finding a house; it’s about securing an investment that fits your life perfectly.

Government Programs and Incentives: Your Financial Toolkit

Every first time home buyer ontario has access to a suite of financial tools designed to lower the barrier to entry. In 2026, the landscape is more favorable than many realize. By combining federal and provincial programs, you can significantly reduce your tax burden while accelerating your savings. It’s not just about finding the money; it’s about using the right sequence of accounts to maximize every dollar. This analytical approach ensures your down payment works as hard as possible before you even sign an offer.

The First Home Savings Account (FHSA) stands as the current gold standard for tax-free growth. You can contribute up to $8,000 annually, with a lifetime cap of $40,000. These contributions are tax-deductible, which lowers your taxable income today. When you’re ready to buy, the withdrawals are entirely tax-free. If you need a larger sum, the Home Buyers’ Plan (HBP) allows you to withdraw up to $60,000 from your RRSP. For couples, this means a combined $120,000 is available for your purchase. These funds must be repaid to your RRSP over a 15-year period, beginning the second year after your withdrawal.

FHSA vs. RRSP: Which Should You Prioritize?

Choosing where to put your money first depends on your unique financial timeline. The FHSA offers the best of both worlds: a tax deduction now and no tax on the growth or withdrawal later. However, the HBP provides immediate access to larger sums if you’ve already built up your RRSP. Pair these accounts strategically. By maximizing both, you can reach a 20% down payment faster and avoid the added cost of mortgage default insurance. This level of planning is a core part of how we help clients redefine their real estate expectations.

Provincial and Municipal Land Transfer Tax Rebates

The Ontario Land Transfer Tax Rebate can save you up to $4,000 on closing day. This covers the full tax on homes priced up to $368,000. For properties above that, the rebate is applied against the total tax owed. If you’re looking in the City of Toronto, you may also qualify for an additional municipal rebate of up to $4,475. In communities like Uxbridge, you’ll only deal with the provincial side, which simplifies your closing costs.

Don’t overlook the First-Time Home Buyers’ Tax Credit (HBTC), which provides a $1,500 federal tax reduction. Additionally, the first-time home buyers’ rebate for GST/HST offers up to $50,000 off the federal portion of the HST for newly constructed homes. When combined with the Ontario Enhanced HST Rebate of up to $130,000, the savings on a new build are substantial. We ensure you don’t miss these critical deadlines or paperwork requirements during the excitement of closing.

The Noble Approach to Financial Readiness and Mortgages

Viewing a mortgage as a simple loan is a common mistake; viewing it as a strategic component of your net worth is the Noble Approach. With a background as a CPA and CA, I help you look past the monthly payment to see the long term investment potential. Every first time home buyer ontario needs this level of analytical rigour. It’s about ensuring your debt load is sustainable, especially with the Bank of Canada policy rate at 2.25% as of May 2026. This professional perspective turns a complex financial decision into a stress-free path toward ownership.

Success in a competitive market like the Durham Region requires more than just a casual interest. You must understand the difference between being pre-qualified and pre-approved. A pre-qualification is a surface-level estimate. A pre-approval involves a deep dive into your credit history and income. It provides a guaranteed rate for a set period and proves to sellers that you’re a serious, capable buyer. In a market where inventory remains a challenge, this distinction can be the deciding factor in a winning offer.

Beyond the Down Payment: Closing Cost Checklist

Budgeting for a home involves more than just the purchase price. We recommend setting aside 1.5% to 4% of the home’s value for closing costs. This ensures you aren’t caught off guard on move-in day. For those considering new constructions, the Ontario HST Rebate for New Homes is a critical piece of the financial puzzle that can significantly offset your initial expenses. Consider these essential costs:

- Home Inspection: This is a non-negotiable investment in your peace of mind. It identifies potential structural or mechanical issues before they become your problem.

- Legal Fees and Title Insurance: A lawyer ensures the title is clear and the transfer is legal. Title insurance protects you against future ownership disputes or fraud.

- Adjustments: You’ll need to reimburse the seller for any prepaid property taxes or utility costs they’ve already covered for the period after you take possession.

Mortgage Structures for First-Time Buyers

Choosing the right mortgage structure is about risk management. As of late April 2026, the lowest 5-year fixed-rate mortgage was 4.04%, while variable rates sat lower at 3.35%. A variable rate might offer lower initial payments, but it requires the stomach for potential fluctuations. If you’re putting down less than 20%, you’ll also need to factor in CMHC insurance premiums. While this adds to the loan amount, it allows you to enter the market sooner. Balancing your amortization period is equally important. A 25-year or 30-year term can lower monthly payments, though it increases the total interest paid over the life of the loan. Our goal is to find the structure that supports your lifestyle while protecting your financial future.

Finding Your Home in Uxbridge and the Durham Region

The search for a home often begins with a compromise between location and budget. In 2026, many people are looking beyond the dense core of the GTA toward the Durham Region, where the average home price sat at $847,776 in April 2026. This area offers a distinct advantage for a first time home buyer ontario because it currently operates as a buyer’s market with 3.5 months of inventory. This breathing room allows you to make decisions based on value and long term potential rather than rushing into a bidding war. Through the Noble Approach, we help you filter MLS listings to find properties that aren’t just houses, but resilient financial assets.

Local expertise is your greatest asset in a shifting market. While national data provides a broad stroke, micro-markets like Uxbridge behave differently. For instance, the average sale price in Uxbridge reached $1,333,667 in February 2026, driven by strong activity in the upper price ranges. Understanding these nuances ensures you don’t overpay or miss out on a community that aligns with your lifestyle goals. We focus on an end-to-end approach that considers everything from property tax rates to future neighborhood development.

Uxbridge: A Community Profile for New Homeowners

Uxbridge is widely known as the Trail Capital of Canada, offering over 220 kilometers of managed trails. This lifestyle appeal is a major draw for young professionals and families who want to balance nature with modern amenities. The downtown core is filled with local cafes and boutique shops, creating a sense of community that’s often missing in larger urban centers. For commuters, the reality is manageable. Transit links and highway access provide reliable routes into the city, making it possible to enjoy a quieter pace of life without sacrificing career growth. You can explore a unique local perspective in our guide to Goodwood, Canada: A Guide to Life in the Real Schitt’s Creek.

Identifying “High-Potential” Properties

When evaluating homes, you must weigh the pros and cons of freehold properties versus condominiums. Freehold ownership gives you full rights to the land and structure, but you’re responsible for all maintenance. Condos offer a lower entry price and shared maintenance, though you’ll need to budget for monthly fees that impact your GDS ratio. During a walkthrough, look for signs of a well-maintained home, such as a modern electrical panel, a dry basement, and a roof in good repair. These details prevent hidden costs after closing. For specific listing strategies, consult our Houses for Sale in Uxbridge: A Buyer’s Guide to refine your search. If you’re ready to see what’s currently available, view my current listings today.

From Offer to Closing: A Stress-Free Path to Ownership

Moving from the search phase to a formal offer is the most critical transition for a first time home buyer ontario. It’s where your financial preparation meets real-world action. Crafting a winning offer involves more than just selecting a price; it requires a strategic balance of conditions that protect your interests while remaining attractive to the seller. Through the Noble Approach, we analyze current market data to ensure your offer is both competitive and fiscally responsible. This structured methodology removes the guesswork, turning a high-pressure moment into a clear, manageable step toward your goals.

Negotiation is an art backed by analytical rigour. Your choice of agent is paramount here, as they act as your primary advocate during complex back-and-forth discussions. Once an offer is accepted, you enter the conditional period. This is your essential window for due diligence. It includes home inspections, title searches, and securing final financing approval from your lender. Given that many mortgage holders face renewals and higher payments in 2026, verifying your financing during this stage is a non-negotiable safety net. We guide you through every inspection report and bank document, ensuring you feel confident before the deal becomes firm.

The Anatomy of an Agreement of Purchase and Sale

The Agreement of Purchase and Sale is the legal foundation of your transaction. Every Ontario buyer should be familiar with standard clauses regarding fixtures, chattels, and the irrevocable period. This period is the timeframe during which your offer remains valid and cannot be withdrawn. In competitive scenarios, the timing of your irrevocable period can be a strategic tool. We also use specific conditions to protect your deposit. This ensures that if a home inspection reveals a major structural flaw or financing terms change unexpectedly, you can exit the agreement with your deposit intact.

Why a Dedicated Buyer’s Agent is Essential

A dedicated buyer’s agent owes you a fiduciary duty. This means they’re legally and ethically bound to act in your best interest at all times. This level of protection is vital, especially when navigating the high stakes of the Durham Region market. Professional representation reduces the stress of the journey by managing timelines, coordinating with lawyers, and providing a seasoned perspective on property value. To ensure you have the right advocate by your side, read Finding the Right Fit: A Guide to Choosing Real Estate Agents Near You to start your search. Closing day is the culmination of this process. It’s the day the legal title transfers, funds are exchanged, and you finally receive the keys to your first home.

Take the First Step Toward Your Future in Ontario

Owning your first home in the Durham Region is more than a personal milestone; it’s a strategic financial decision that builds long term security. By mastering the 2026 landscape, you can turn current market trends into a distinct advantage. You now have the knowledge to maximize the $8,000 annual FHSA contribution and claim your $4,000 provincial land transfer tax rebate with total confidence. As a first time home buyer ontario, you deserve a process that is as rewarding as the destination.

My background as a CPA and CA provides the analytical rigour needed to navigate mortgage structures and closing costs without the stress. We combine this financial expertise with deep-rooted knowledge of Uxbridge and the surrounding areas to ensure you find a home that offers genuine value. Redefine your expectations and start your home search with The Noble Approach today. Your path to homeownership is clear, and we’re here to ensure every step is handled with the utmost care and professional excellence. We look forward to helping you secure your future.

Frequently Asked Questions

How much down payment do I need for a first home in Ontario?

You need a minimum of 5% on the first $500,000 and 10% on any amount between $500,000 and $999,999. For a home at the Durham Region average price of $847,776 in April 2026, this equals a down payment of approximately $59,778. If the purchase price is $1,000,000 or more, a full 20% down payment is required. We analyze these ratios carefully to ensure your monthly cash flow remains sustainable.

Can I use the FHSA and HBP at the same time?

Yes, you can combine both the First Home Savings Account (FHSA) and the Home Buyers’ Plan (HBP) for a single purchase. This is a powerful strategy for a first time home buyer ontario in 2026. By using the $40,000 FHSA lifetime limit and the $60,000 HBP withdrawal, an individual can access $100,000 in tax-advantaged funds. Couples can double this to $200,000 to reach a 20% down payment faster.

What is the maximum house price for the Ontario Land Transfer Tax rebate?

There is no maximum house price for eligibility, but the rebate is capped at $4,000. This amount completely offsets the provincial land transfer tax for homes priced at $368,333 or less. For properties above this value, such as an average Uxbridge home at $995,779, you’ll still receive the full $4,000 credit against the total tax owed at closing. This helps reduce your immediate cash requirements on move-in day.

Is a home inspection mandatory for first-time buyers?

A home inspection isn’t legally required, but we consider it a non-negotiable step in the Noble Approach. In the current Durham Region buyer’s market, which has 3.5 months of inventory as of April 2026, including an inspection condition is a standard way to protect your investment. It identifies hidden structural or mechanical issues before you’re legally committed, ensuring your path to ownership remains stress-free and predictable.

How much are closing costs typically in the Durham Region?

You should budget between 1.5% and 4% of the purchase price for closing costs. On an average Durham home priced at $847,776, this ranges from roughly $12,716 to $33,911. These costs cover legal fees, title insurance, home inspections, and land transfer taxes. We provide a detailed, analytical breakdown early in the process so you can manage your savings with the precision of a finance professional.

Does a first-time buyer pay GST/HST on a house in Ontario?

You don’t pay GST/HST on the purchase of a resale home. However, new constructions are subject to these taxes. For agreements signed between April 1, 2026, and March 31, 2027, the Ontario Enhanced HST Rebate can remove the full 13% HST on eligible homes up to $1 million. The federal first time home buyer ontario GST/HST rebate also offers up to $50,000 in additional savings for newly built properties.

What happens if I decide to rent out my first home later?

You can rent out the property eventually, but you must occupy it as your principal residence first to qualify for most incentives. Rebates like the land transfer tax credit and HST rebates typically require you to live in the home for at least one year. If you move out or rent it sooner, the government may require you to repay a portion of those tax savings. We help you plan for these long term transitions.

How do I qualify for the First-Time Home Buyers’ Tax Credit?

To qualify, you or your spouse must acquire a qualifying home and not have lived in another home owned by either of you in the current or previous four years. You claim this on your annual tax return to receive a non-refundable credit that reduces your federal income tax by up to $1,500. It is a straightforward way to recoup some of your initial costs after your first year of homeownership.