Looking For More Great Content?

Get even more informative Toronto real estate news sent directly to your inbox by signing up for my newsletter here. All it takes is a few easy clicks.

How to Sell and Buy a House at the Same Time: The 2026 Strategic Guide

04/24/26 Uncategorized

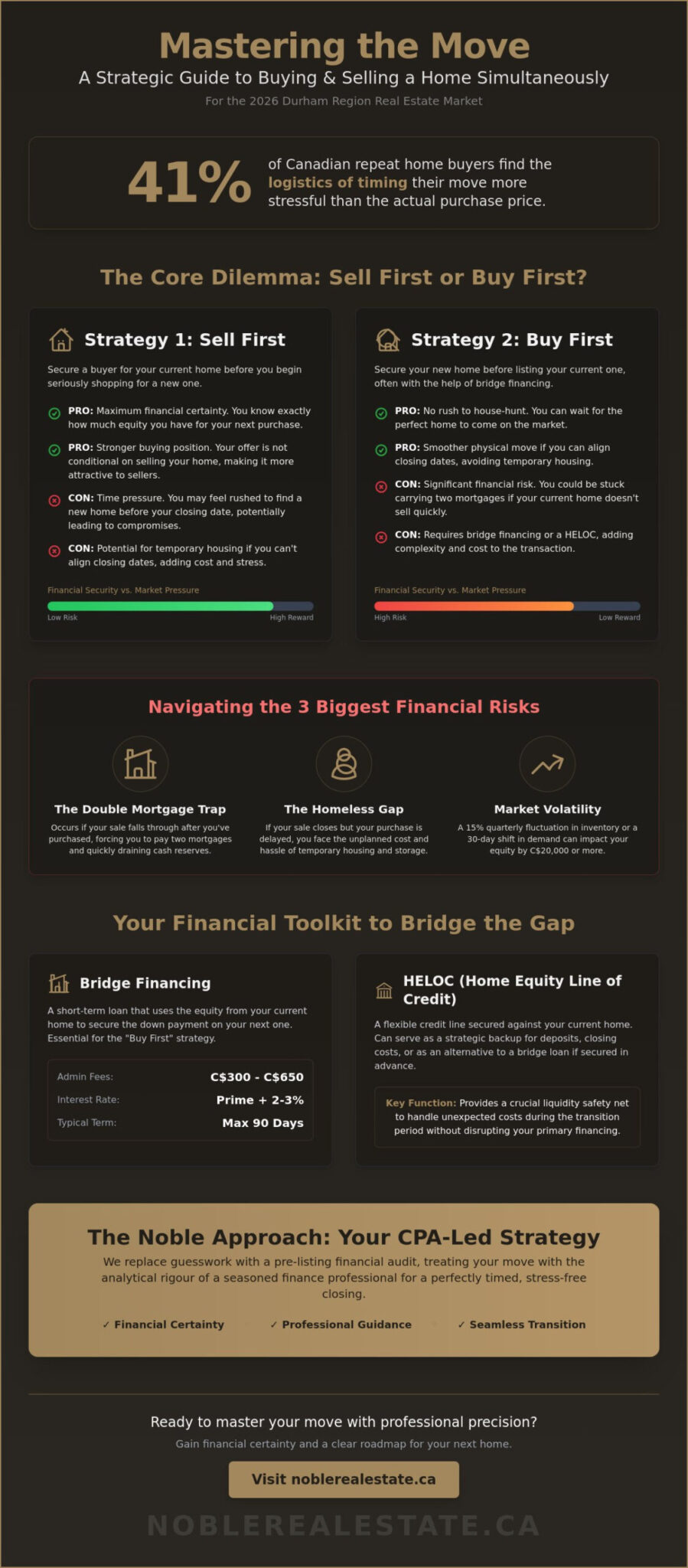

What if the most complex financial move you ever make could be handled with the precision of a professional audit? A 2024 survey of Canadian homeowners revealed that 41% of repeat buyers find the logistics of timing a move more stressful than the actual purchase price. Learning how to sell and buy a house at the same time often feels like a high-stakes gamble where your equity is on the line. You’re likely feeling the weight of potential bridge financing costs or the fear of being stuck with two mortgages if your timing misses the mark by even a few days.

We agree that your hard-earned equity deserves more protection than a “wait and see” strategy provides. This 2026 strategic guide offers a clear, expert-led roadmap to help you master the logistics of simultaneous transactions. By applying the Noble Approach, you’ll gain the financial certainty and professional guidance needed for a perfectly timed closing. We will break down everything from coordinating possession dates to managing the analytical side of bridge loans, ensuring your move-up or downsize is a stress-free success.

Key Takeaways

- Navigate the 2026 Durham Region market with a clear understanding of the logistical “buy and sell dance” to minimize stress and maximize timing.

- Master the financial mechanics of how to sell and buy a house at the same time using strategic tools like bridge financing and HELOCs tailored for the Canadian market.

- Evaluate the “Sell First” versus “Buy First” strategies to identify which tactical path offers the right balance of financial security and house-hunting freedom for your family.

- Implement the “Noble CPA Method” for a pre-listing financial audit, ensuring every transaction is backed by the analytical rigour of a seasoned finance professional.

- Follow a structured 5-step roadmap designed to redefine your expectations and provide a seamless transition between your current home and your next local investment.

The Complexity of Simultaneous Real Estate Transactions in 2026

Entering the 2026 market in Durham Region requires more than just luck; it requires a high-stakes coordination of two distinct moving parts. You’re likely trying to figure out how to sell and buy a house at the same time without risking your financial stability. This “buy and sell” dance is often the most stressful event in a homeowner’s life. It forces you into a psychological “Entry State,” where you’re caught between the excitement of a new beginning and the heavy logistical burden of your current property. The pressure to time these events perfectly can feel overwhelming if you don’t have a clear roadmap.

At Noble Real Estate, we address this complexity through “The Noble Approach.” This methodology isn’t just about finding a buyer. It’s about applying analytical rigour and professional financial planning to your specific timeline. Market conditions in 2026 have shown that inventory levels in communities like Whitby and Oshawa can fluctuate by 15% within a single quarter. This volatility means precision matters more than ever. We focus on reducing your stress by treating your transition with the same care as a corporate merger, ensuring every financial detail is secured before you commit to a move.

The Three Biggest Risks of Concurrent Moving

- The Double Mortgage Trap: This occurs if your sale falls through after you’ve already committed to a new purchase. You could find yourself responsible for two monthly payments, which quickly drains your cash reserves.

- The Homeless Gap: If your purchase closing date is delayed but your sale proceeds as planned, you might need temporary housing and storage for your belongings.

- Market Volatility: A 30-day shift in local demand can impact your equity position by C$20,000 or more. A foundational part of mitigating these risks involves understanding real estate contracts and the specific legal contingencies that protect your deposit during a bridge period.

Why Ontario’s Rules Make Timing Critical

In Ontario, your cash flow is heavily impacted by the Land Transfer Tax. On a C$1,000,000 purchase, you might face approximately C$16,475 in provincial taxes. This makes liquidity a vital part of your strategy. Current uxbridge real estate trends indicate that whether you should list or look first depends entirely on the specific inventory levels in your neighborhood. Your real estate lawyer plays a central role in this process, as they must coordinate the simultaneous transfer of funds and titles. Mastering how to sell and buy a house at the same time in 2026 means having an advisor who understands these legal and financial nuances inside and out.

Financial Strategies to Bridge the Gap

Managing two major transactions simultaneously requires more than just luck; it demands a calculated financial roadmap. My “Noble Approach” integrates a CPA’s analytical rigour to ensure you aren’t left overextended if timelines shift. Successfully learning how to sell and buy a house at the same time involves understanding that your equity is often temporarily trapped between two front doors. To navigate this, we look at liquidity tools that provide a safety net without compromising your long-term solvency.

Beyond bridge loans, a Home Equity Line of Credit (HELOC) serves as a strategic backup. If you secured a HELOC while your current home was unencumbered by a pending sale, those funds can cover unexpected closing costs or deposits. However, 2026 regulations require strict debt-service ratios. I recommend a “worst-case” stress test: calculating your ability to carry both mortgages for 120 days. This ensures that even if a buyer’s financing falters, your transition remains secure and stress-free and straightforward.

How Bridge Loans Work in Ontario

Bridge financing is a short-term debt instrument used until a permanent loan is secured. In the Ontario market, lenders typically facilitate this when you have a firm Sale and Purchase Agreement for both your current and future properties. The mechanics are simple: the lender advances the equity from House A to close on House B before the first sale officially completes. In 2026, expect administration fees to range between C$300 and C$650, with interest rates typically sitting at Prime plus 2% or 3%. Most lenders limit these loans to a 90-day term, making them a precise tool for tight transitions rather than a long-term solution.

Leveraging the ‘Sale of Property’ Condition

The Sale of Property (SOP) condition is a powerful protective layer for buyers. It makes your purchase of a new home contingent on the successful sale of your current one. While this protects your capital, it can make your offer less attractive in competitive areas like Uxbridge. To balance this, we often include an “Escape Clause.” This gives the seller the right to continue showing the home. If they receive a better offer, you are given a 48-hour or 72-hour window to either remove your conditions or walk away with your deposit intact.

To make an SOP offer stand out in 2026, transparency is vital. We provide the seller with a comprehensive marketing plan for your current home and a professional valuation. Showing that your home is priced to sell quickly reduces the seller’s perceived risk. This level of preparation is a hallmark of how to sell and buy a house at the same time while maintaining a position of strength at the negotiating table. We focus on creating a “win-win” scenario where the seller feels confident in your ability to perform.

Buying First vs. Selling First: A Tactical Comparison

Deciding whether to list your current property or secure a new one first is the most significant hurdle when learning how to sell and buy a house at the same time. This choice dictates your financial exposure and your daily stress levels during the transition. The Noble Approach applies a rigorous, analytical lens to this decision, ensuring your equity remains protected throughout the process. We prioritize your financial health by weighing the risks of the Durham Region market against your personal goals.

The Case for Selling First

Selling your home before committing to a new purchase provides the highest level of financial certainty. You’ll know the exact net proceeds from your sale, which eliminates the guesswork from your next purchase budget. This strategy removes the need for bridge financing, which in 2025 and 2026 often carries interest rates 1% to 2% above the bank prime rate. However, the logistical pressure is higher. If your home sells quickly, you might face a 60-day closing window to find and buy a new property. This often leads to “double-moving” costs. Families might need to rent short-term storage and temporary housing, adding roughly C$3,500 to C$6,000 to the total move cost.

- Pros: Absolute budget clarity; no risk of carrying two mortgages.

- Cons: Intense time pressure; potential for two moves.

- Ideal for: Conservative movers and those with strict debt-to-income ratios.

The Case for Buying First

Buying first allows you to wait for a home that truly fits your criteria in Uxbridge or the surrounding areas. You only move once. This saves significant time and emotional energy. The risk is purely financial. If your current home doesn’t sell as quickly as anticipated, you could be responsible for two mortgage payments simultaneously. In a shifting market, this might force a “fire sale” where you accept an offer 5% to 8% below market value just to offload the debt. This path requires significant equity or a robust line of credit to manage the overlap. It’s a strategy for those who value the “perfect” home over immediate liquidity.

- Pros: Stress-free house hunting; single move.

- Cons: High financial risk; bridge loan interest costs.

- Ideal for: Buyers in fast-moving seller’s markets with high home equity.

We often explore middle-ground solutions like the “Rent-Back” agreement. This involves selling your home but negotiating a clause to stay as a tenant for 30 to 90 days after closing. It provides the cash you need for your next purchase while giving you a buffer to shop without the fear of being homeless. In the Durham Region, where inventory levels fluctuated by 14% last year, having this flexibility is a vital tactical advantage when figuring out how to sell and buy a house at the same time. This approach turns a complex transition into a structured, manageable plan.

The 5-Step Roadmap for a Seamless Transition

Mastering how to sell and buy a house at the same time requires a disciplined schedule and a focus on financial logic. This process isn’t about luck; it’s about sequence. By following a structured roadmap, you can minimize the risk of being “homeless” or carrying two mortgages longer than necessary.

- Step 1: The Pre-Listing Financial Audit (The Noble CPA Method). We begin with a rigorous analysis of your equity. This involves calculating your net proceeds after C$ mortgage discharge fees, legal costs, and real estate commissions. We don’t guess. We provide a clear C$ figure so your next purchase is grounded in reality.

- Step 2: Securing Conditional Pre-Approval. Lenders in 2026 require specific documentation for concurrent transactions. You need a pre-approval that accounts for bridge financing. This ensures you have the liquidity to deposit on a new home before the funds from your current sale are released.

- Step 3: Strategically Timing Your Listing. We analyze market absorption rates in your specific neighborhood. If the average home in your area sells in 15 days, we time your listing to ensure your sale is firm before you make an unconditional offer on your next property.

- Step 4: Aligning Closing Dates. We use the ‘Perfect Friday’ strategy. This involves staggering your closing dates to avoid the logistical nightmare of a same-day move.

- Step 5: Executing the Move with a Contingency Buffer. We recommend a C$15,000 liquidity buffer to cover potential delays or short-term storage. This protects your peace of mind if a buyer requests a 48-hour extension.

Coordinating the Closing Dates

A same-day closing is often the most stressful way to move. We recommend a 2-3 day overlap instead. This allows you to clean and paint your new home before the moving truck arrives. While you are exploring houses for sale in uxbridge, we focus on securing a “clean” deal for your current home. A buyer with a massive down payment and firm financing is more valuable than a higher offer with shaky mortgage conditions.

The Noble Approach to Preparation

Our team uses analytical data to predict exactly how long your home will sit on the market based on current inventory levels and interest rate trends. We don’t wait for the “For Sale” sign to start working. Our pre-marketing strategies build heat through targeted digital campaigns 10 days before you go live. The Noble Approach is a financially-driven real estate methodology that prioritizes client equity and peace of mind.

Planning a complex move requires more than just a realtor; it requires a financial strategist. Connect with Noble Real Estate today to see how we can simplify your transition.

Redefining Expectations: Why The Noble Approach Works

Real estate transactions involve significant capital, often representing the largest portion of a family’s net worth. Colin Noble brings a unique advantage to the table as a CPA and CA. This financial background ensures that every decision is backed by analytical rigour and professional scrutiny. When you’re figuring out how to sell and buy a house at the same time, the margin for error is slim. The Noble Approach focuses on precision, ensuring your equity is protected while you transition from your current property to your next home in Uxbridge or the Durham Region.

Client success stories highlight the effectiveness of this methodology. One recent family in Durham managed to close both their sale and purchase within a 24-hour window, avoiding the C$3,000 to C$7,000 costs often associated with extended bridge financing or temporary storage. We prioritize a stress-free, straightforward experience by managing the logistical moving parts that often overwhelm homeowners. Our local expertise allows us to anticipate market shifts in Ontario, ensuring your timing is optimized for the best possible financial outcome.

- Analytical financial oversight from a CPA/CA perspective

- Deep roots and market knowledge in Uxbridge and Durham Region

- Proven track record of managing simultaneous closings

- Commitment to a transparent, advisory-led process

Expertise That Goes Beyond the MLS

Most real estate agents near me provide a standard listing service, but a complex move requires a deeper advisory partnership. We look past the surface of a transaction to identify potential hidden costs like land transfer taxes, legal disbursements, and unexpected inspection repairs. Our goal is to minimize these financial surprises before they impact your bottom line. By providing a full-service, end-to-end approach, we ensure you aren’t just moving houses; you’re making a sound investment. We handle the data so you can focus on the excitement of your new home.

Start Your Journey Today

Moving up in the Ontario market doesn’t have to be a source of anxiety. We invite you to a complimentary “Simultaneous Move” strategy session where we’ll map out your specific timeline and financial goals. You can begin the process by using our Home Valuation tool to establish your current market position. This is the first step toward a seamless transition and a successful closing. It’s time to Redefine your real estate expectations with Colin Noble and discover how a professional, financially savvy approach makes all the difference when learning how to sell and buy a house at the same time.

Take Command of Your 2026 Move

Navigating the Canadian real estate market requires a blend of local insight and financial rigour. You’ve learned that balancing two transactions isn’t just about timing; it’s about leveraging the right bridge financing and a structured five step roadmap. Successfully mastering how to sell and buy a house at the same time comes down to removing the guesswork from the equation. By prioritizing a strategic path based on your specific liquidity needs, you can transition to your next home without the typical industry friction.

With a professional background as a CPA and CA, I provide the analytical depth needed to protect your equity during these complex transitions. My stress free system, known as The Noble Approach, is designed specifically for the Uxbridge area to ensure your move is both profitable and predictable. We’ll look at the data, align your timelines, and execute a plan that focuses on your goals. It’s time to trade uncertainty for a clear, professional path forward.

Ready to secure your future home with confidence? Book Your Strategic Move-Up Consultation with Colin Noble today. Your seamless transition starts with a single conversation.

Frequently Asked Questions

Can I actually buy a new home before my current one is sold?

Yes, you can buy a new home before selling your current one, and it’s a common strategy in the Ontario market. The Noble Approach focuses on using a “Sale of Property” condition in your offer to protect your deposit if your current home doesn’t sell within a specific timeframe. This method ensures you have a guaranteed place to live before you commit to leaving your existing residence.

What is a bridge loan and how much does it typically cost in Ontario?

A bridge loan is a short term financing tool that lets you use the equity from your current home to pay for your new one before the first sale closes. In Ontario, major banks typically charge interest rates around Prime plus 2% or 3%, with administrative fees between C$200 and C$500. It’s a practical way to manage the financial gap when closing dates don’t align perfectly.

What happens if my house doesn’t sell by the time I need to close on my new one?

If your home hasn’t sold by your new closing date, you’ll need to rely on bridge financing or a private loan to cover the temporary ownership of two properties. Most Canadian lenders require a firm sale agreement to approve a bridge loan, which usually lasts up to 90 days. We help you monitor market data closely to ensure your listing is priced to move within your required timeline.

Is it better to have a long or short closing period when doing both at once?

A longer closing period of 60 to 90 days is generally better because it provides a necessary buffer to find the right buyer for your current property. Shorter windows of 30 days often lead to increased stress and might force you to accept a lower offer just to meet a deadline. When you’re learning how to sell and buy a house at the same time, extra time is your most valuable asset.

How do I handle the Land Transfer Tax when I’m buying and selling simultaneously?

You must pay the Land Transfer Tax on the property you’re purchasing, but there’s no tax to pay on the one you’re selling. In Ontario, the tax is calculated on a sliding scale, such as 1.0% on the amount between C$55,000 and C$250,000. These funds are due on closing day, so it’s vital to have this cash ready in your lawyer’s trust account.

Can I use the equity in my current home for the down payment on the next one?

You can use your equity for a down payment by setting up a bridge loan or a Home Equity Line of Credit (HELOC). Per OSFI regulations, you can access up to 80% of your home’s value through a HELOC. This strategy is a fundamental part of how to sell and buy a house at the same time, allowing you to secure your next home without needing a massive cash reserve.

What is a ‘Rent-Back’ agreement and how can it help me?

A rent-back agreement is a clause where you sell your home but stay there as a tenant for a short period after the closing date. This usually lasts for 30 days or less and helps you avoid moving twice if your new home isn’t quite ready. It’s an excellent tool for reducing moving day logistics and keeping your transition as straightforward as possible.

How do I qualify for a mortgage on a second home while still owning my first?

Lenders qualify you for a second mortgage by analyzing your Total Debt Service (TDS) ratio to ensure you can handle the carry costs of both homes. Most Canadian financial institutions want your total debt obligations to stay below 44% of your gross household income. Our team’s financial background helps you run these numbers early so you can move forward with professional confidence.